The Evolving Nature of Global Trade: An Analysis of Time Varying Volatility, Conditional Correlations and Elasticities (1990- 2024)

Abstract

This paper examines the evolution of global trade dynamics analyzing data for 213 countries from 1990-2024 using the World Banks’ World Development indicators. We focus on the time varying nature of trade elasticities, conditional correlations and structural heterogeneity across countries and sectors. An integrated time series econometric pipeline is implemented combining GARCH (1,1) models, rolling volatility measures and dynamic correlation analysis. We document the following fundamental transformations.

First, volatility persistence has reached financial market levels, the GARCH estimates reveal goods exports volatility exhibits near unit root persistence (α+β = 0.93), indicating that shocks decay slowly with long lasting effects, this is supported by a realized volatility year to year persistence of 0.63. Service goods exports show an integrated GARCH process (β = 1.0000) indicating permanent volatility shocks. Trade volatility increased 87.4% post 2008 while GDP volatility decreased 21.4%, creating an unprecedented volatility gap.

Second, Trade-GDP linkages have weakened structurally, Rolling correlation analysis shows that trade and GDP shocks shifted from -0.40 pre 2008 to -0.06 post 2008 indicating a -0.34 point decline confirmed by Chow testing (F=15.4, p=0.03). Crisis responses show remarkable heterogeneity, ranging from extreme synchronization during the Global Financial Crisis (2009 correlation: -0.89) to partial decoupling during the COVID-19 pandemic (2020: -0.42).

Third, we identify an inverted U relationship between trade openness and crisis resilience, Optimal crisis outcomes occur at moderate trade openness (30-60% of GDP), with both lower and higher openness increasing vulnerability. Service dominant economies exhibit superior crisis performance (-1.20% average GDP impact versus -1.81% for goods-dominant), suggesting services trade offers stability alongside growth.

Fourth, Random Effects regression reveal that GDP growth remains the primary driver of exports (elasticity 0.65), while inflation consistently reduces export performance. Exchange rate levels have no significant effect on total exports(p=0.83). however, exchange rate volatility significantly reduces goods exports (β =-7.837e-06, p =0.04) but has no effect on services p=0.64), confirming a dual trade system.

These findings challenge constant parameter trade models and have immediate policy implications: openness strategies should target optimal rather than maximal levels, stabilization frameworks require longer horizons given volatility persistence, and services development can enhance both growth and stability. Our results establish that understanding time-varying dynamics is essential for navigating the recomposed globalization of the 21st century.

1. INTRODUCTION:

1.1 Trade Integration and Structural Instability

The period from 1990 to the mid-2000s has been labelled an era of hyper globalization. It was characterized by the rise of global value chains (GVCs), rapid trade liberalization, expanding trade volumes and falling costs of trade (Rodrik ,2eng018). Using instrumental variables to address endogeneity, Frankel and Romer (1999) estimated that a 1% increase in trade openness raised income per capita by roughly 0.5-2%. This finding become a basis of development policy, justifying various aspects from WTO accession to structural adjustment programs. Yet the consensus began to take shape only after 2008.

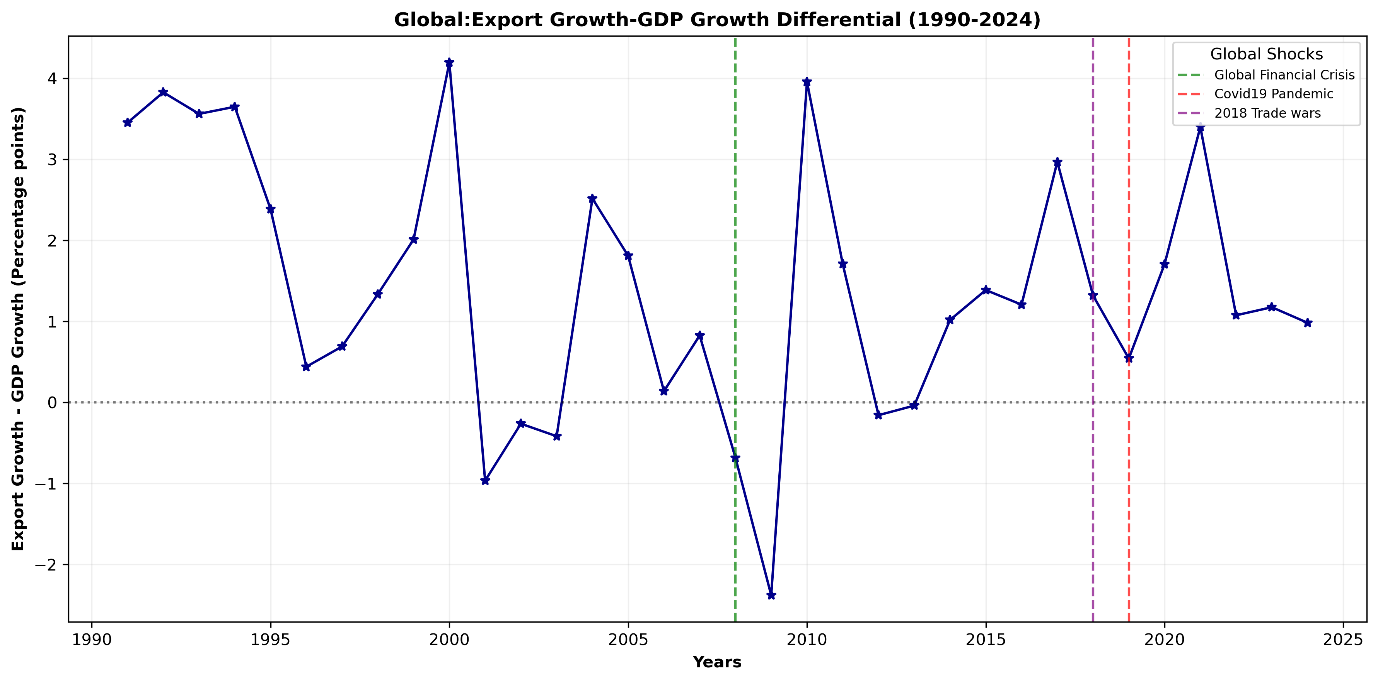

The 2008 Global Financial Crisis triggered the so called ‘Great Trade Collapse’, this was defined by a structural break and a temporary contraction in the trade and growth linkage which never fully recovered their prior expansionary phase relative to output. (Freund 2009). Subsequent shocks as shown in Figure 1, notably, the US-China trade war (2018-2020), Covid19 pandemic induced supply disruptions and geopolitical realignments further exposed the fragile nature of deeply integrated systems. Currently, global trade is characterized by significant volatility, where risks emerge from within the system itself and its connection to macroeconomic fundamentals is not fixed

Figure 1: Global Trade -GDP Growth Differential (Exports Growth-GDP Growth), 1990-2024

In finance, ignoring volatility dynamics leads to mis specified risk assessments and flawed policy prescriptions (Engle,2002). The same logic now applies to trade, the shocks and transformation in trade demand new analyses that move beyond static elasticities and constant variances to model time varying uncertainty, persistence and conditional dependence.

1.2 The Gap Between Empirical Reality and Standard Models

Much of the trade literature remains anchored in frameworks unsuitable for the volatility nature of trade despite mounting evidence of instability. Gravity models assume stable bilateral relationships and ignore time varying heteroskedasticity (Head & Mayer, 2014). Dynamic Stochastic General Equilibrium (DSGE) Open economy models impose constant trade elasticities and exogenous shock processes (Justiniano et al., 2011). Panel regressions treat coefficients as fixed across decades, masking structural evolution.

These approaches, while practical they can obscure a significant flaw. They fail to answer three urgent questions:

1. Does trade volatility exhibit clustering and persistence similar to financial markets and has this intensified post 2008?

2. How have the conditional correlations between trade and GDP evolved, and what explains the apparent decoupling in recent years?

3. Are there systematic differences in volatility and resilience between goods and services, or across income groups?

Table 1: Summary of Key Facts: Global Trade Dynamics Pre vs.Post the 2008 Global Financial Crisis

| Metric | Pre 2008 | Post 2008 | Change |

|---|---|---|---|

| Average trade volatility (5-year rolling std.dev.) | 0.06 | 0.112 | +87.4% |

| Average GDP volatility (5-year rolling std.dev.) | 0.098 | 0.077 | -21.4% |

| Dynamic correlation: Exports vs. GDP growth | -0.40 | -0.06 | +0.34 pts |

| Trade- GDP growth differential(pp) | +2.29 | +3.94 | +1.65pp |

| Crisis GDP impact (openness>60% of GDP) | - | -2.11% | worse than moderate openness |

Volatility measures are 5-year rolling standard deviations of annual growth rates. Dynamic correlation is the average time varying (DCC GARCH) correlation between export and GDP contraction during 2008-2009 for countries with trade openness above 60% of GDP.

Source: Authors calculations based on World Development Indicators (World Bank,2024).

The answers to these questions matter for both academic completeness and practical decision making. For policy makers, misjudging volatility persistence can lead to undercapitalized stabilization funds or ineffective countercyclical buffers. For businesses, assuming stable trade GDP linkages risks flawed supply chain design and for multilateral institutions, outdated models may misdiagnose the roots of trade stagnation.

1.3 Contributions

The study therefore addresses these gaps through a comprehensive analysis of global trade dynamics from 1990 to 2024, using data from the World Banks’ World Development Indicators for 213 countries. Our contribution is threefold:

Methodologically, we implement an integrated analytical workflow that scales from data exploration and stationarity testing to advanced time series econometrics. We employ both parametric (GARCH models) and nonparametric (rolling windows) approaches to volatility estimation, we estimate time varying correlations using both conditional correlation models and rolling correlations providing consistent evidence across different analytical methods.

Empirically, we document several findings that differ from established expectations:

First, we discover extreme volatility persistence, the GARCH models reveal that goods export volatility exhibits near unit root persistence (α+β = 0.93), implying that shocks decay slowly with long lasting effects, while services trade follows an integrated GARCH process (β= 1.0000) with permanent volatility effects.

Second, a structural break was identified in 2008, the Chow test confirms a regime shift (F=15.4, p=0.00), with trade volatility increasing 87.4% post 2008 while dynamic correlation with GDP weakened from -0.40 to -0.06 (Table 1).

Third, we identify a non-linear relationship between trade openness and crisis resilience. Countries with moderate openness 30-60% of GDP were found to deliver the best outcomes challenging both protectionist and hyper globalization narratives.

Fourth, service exports were identified as a trade stabilizer, service dominant economies show superior crisis resilience (-1.11% Trade impact vs -3.94% for goods dominant economies), highlighting the buffering role of digital and intangible trade.

Theoretically, our findings challenge constant parameter assumptions in trade models and suggest the need for frameworks that account for time varying dynamics. The assumption of stable elasticities and exogenous volatility is untenable in a world where risk is endogenously amplified by financial integration, supply chain complexity, and policy uncertainty (IMF, 2023). The evidence of changing transmission mechanisms between trade and GDP, coupled with the extreme persistence of volatility, points toward a need for new theoretical frameworks

1.4 Policy Relevance and Broader Implications

The analysis offers crucial insights for economic theory.

For policymakers, the findings suggest that: Trade stabilization measures need longer horizons given volatility persistence; Services trade development can enhance both growth and stability; Strategic moderate openness may outperform either extreme.

For businesses, the results indicate extended risk management measures and differentiated strategies for goods versus services trade.

For researchers, they highlight the importance of incorporating time varying parameters and volatility dynamics into trade models.

Perhaps most fundamentally, our findings suggest that global trade is not experiencing simple stagnation "slowbalization" as Eichengreen (2015) suggests, but rather structural recomposition with different components (goods vs. services), different country groups, and different time periods exhibiting distinct dynamic properties. Understanding this recomposition is essential for success in the evolving global world.

1.4: Roadmap

The remainder of this paper proceeds as follows. Section 2 reviews relevant literature on trade elasticities, macroeconomic volatility, and time-series econometrics. Section 3 describes our data sources, variable construction, and methodological framework. Section 4 presents our empirical results in logical progression: first documenting structural trends, then analyzing volatility dynamics, followed by time-varying correlations, and finally examining heterogeneity across country types. Section 5 discusses the implications of our findings for economic theory, policy design, and business strategy. Section 6 concludes and suggests directions for future research.

2. LITERATURE REVIEW

2.1 The Evolution of Trade Elasticity Estimation

The Estimation of trade elasticities which measure the responsiveness of trade flows to changes in income, prices and policy has been a crucial part of international economics framework for decades. Frankel and Romer (1999) established a positive link between trade openness and income per capita. Using panel data models with constant parameters over time they estimated an income elasticity of trade near unity. This finding was reinforced by Dollar and Kray (2003), who argued that globalization benefits the poor, further grounding the view of trade as a stable engine of growth. This approach assumes that the income elasticity of trade estimated for the 1990s remains valid in the 2020s, despite profound changes in global value chains, digitalization, and geopolitical fragmentation.

Recent work has begun to acknowledge heterogeneity in these elasticities. (Imbs & Méjean, 2015) documented substantial variation across sectors and product types, while (Araújo & Martins, 2009) tested for structural breaks in import demand functions, finding evidence of parameter instability around major crises. Herzer (2013) used time varying coefficient models to show declining trade growth elasticities in developing countries.

However, this literature has predominantly focused on shifts in first moment parameters i.e. the conditional mean, paying limited attention to changes in second moments i.e. conditional variance and covariance. Our study bridges this gap by modeling how both the magnitude (volatility) and co-movement (correlation) of trade with macroeconomic fundamentals have evolved over three decades.

2.2 Volatility in International Economics:

Volatility modeling originated in finance with Engles (1982) ARCH and Bollerslevs (1986) GARCH models, they captured the tendency of financial shocks to cluster and persist. In macroeconomics, volatility research initially flourished in finance before extending to exchange rates (Andersen et al., 2003) and inflation (Stock & Watson, 2007). This was soon applied to macroeconomic variables. Blanchard and Simon (2001) documented the “Great Moderation” which was a secular decline in U.S. output volatility from the mid-1980s to 2007 attributed to better monetary policy (Stock & Watson, 2002) and inventory management (McConnell & Pérez-Quiros, 2000).

Yet trade volatility has been overlooked on this discussion. Early contributions like di Giovanni and Levchenko (2009) showed that trade intensive sectors exhibit higher output volatility, while Kali et al. (2007) linked openness to volatility in developing economies. However, these analyses primarily used unconditional variances and focused on output rather than trade flows themselves. More recently, IMF (2023) noted rising trade volatility post-2008 but did not model its dynamics.

The conditional, time varying nature of trade volatility clustering, persistence, and regime changes remains underexplored. By adapting financial volatility models to global trade data, we fill this omission in the literature, particularly given our finding of extreme persistence (α+β = 0.93) that approaches financial market levels.

2.3 Time-Varying Correlations and the Transmission of Shocks

The co-movement of economic variables across countries is dynamic. Engles (2002) Dynamic Conditional Correlation (DCC) model transformed the study of time-varying interdependencies in asset markets, allowing correlations to evolve as a function of past shocks and volatilities. In international macroeconomics, DCC and related models have been used to study business cycle synchronization (Kose et al., 2003) and financial contagion (Forbes & Rigobon, 2002).

However, application to trade GDP linkages remains limited. Some studies examine correlations between trade and output growth (Calderón et al., 2007) but report simple rolling unconditional correlations rather than model based conditional correlations that filter out volatility effects. This distinction is crucial, a change in unconditional correlation can be driven either by changing fundamental co-movement or merely by shifting relative volatilities. By employing both DCC-GARCH and rolling correlation approaches, we isolate the evolution of the conditional correlation between trade and GDP shocks, providing clearer evidence of the structural decoupling (-0.40 to -0.06) that has occurred since 2008.

2.4 Distinction Between Services and Goods Trade

Traditional trade theory has been predominantly goods centric, with classical models (Ricardian, Heckscher-Ohlin) focusing on comparative advantage in physical goods production, with services treated as non-tradable. Even new trade theory (Krugman, 1980) focused on differentiated manufactured goods. The growing importance of services trade has challenged this focus

Digitalization has enabled the rise of cross border services. Deardorff (2001) extended comparative advantage logic to services, while Miroudot and Cadestin (2017) documented the growing role of services in GVCs. Empirically, Benz (2017) noted lower volatility in services exports, and Lodefalk (2014) found distinct determinants for services trade. Systematic time series evidence on whether this lower volatility is persistent and how it correlates with global demand is lacking.

Our GARCH results reveal a stark contrast, goods exports follow a highly persistent but stationary process (α + β = 0.93), while services exhibit an integrated GARCH (IGARCH) process (β ≈ 1), implying permanent volatility shocks. This suggests services trade is not merely less volatile but follows a different dynamic where shocks are persistent rather than temporary. These finding challenges existing theory and calls for new models of intangible trade under uncertainty.

2.5 Trade Openness and Economic Resilience

There is a long-standing theoretical debate about trade openness and stability relationship, the diversification theory by Obstfeld (1994) suggests openness buffers country specific shocks by spreading risk across markets through access to multiple markets. The contagion theory by Rodrik (1998) warns that integration amplifies exposure to external crises. Empirical evidence has been mixed. Easterly et al. (2000) found openness increases volatility in developing countries, while Kose et al. (2003) showed complex relationships depending on country characteristics and shock types.

Our finding of an inverted U-shaped relationship with optimal crisis resilience at (30–60% trade openness) implies that diversification benefits dominate at moderate openness, but contagion risks overwhelm them at extremes. This nonlinearity aligns with recent work by Furceri et al. (2020), who found threshold effects in trade growth relationships, but extends it to volatility and crisis impact a dimension previously unexplored.

2.6 Structural Breaks and the End of Hyper globalization

The concept of structural breaks in globalization patterns gained prominence following the 2008 crisis. (Baldwin, 2016) posits that globalization peaked around 2008, giving way to fragmentation. Antràs (2020) documented declining GVC participation, while Evenett and Fritz (2023) tracked rising protectionism.

However, these accounts are largely descriptive or policy-oriented. Formal statistical testing for structural breaks in trade dynamics remains scarce. Helpman et al. (2008) tested for breaks in trade cost elasticities, and Araújo and Martins (2009) in import demand but none examined second moment properties.

Our application of Chow tests (F=15.4, p=0.00) to volatility and correlation series provides formal statistical evidence of a shift in the volatility regime, aligning with broader observations about changing globalization. The alignment of our estimated breakpoint (2008-2009) with the Global Financial Crisis supports theories emphasizing financial real linkages in modern trade. Amiti & Weinstein (2011) showed that trade credit collapse drove the Great Trade Collapse. Suggesting that modern trade is inseparable from financial conditions, a mechanism that would naturally induce persistent volatility shifts.

2.7 Synthesis and Contribution

The existing literature offers strong but fragmented foundations. Trade elasticity models (Frankel & Romer, 1999) ignore time varying risk, volatility frameworks (Engle, 1982) are rarely applied to trade flows, correlation models (Engle, 2002) focus on finance, not real trade linkages, openness resilience studies (Rodrik, 1998) assume linearity and structural break analyses (Baldwin, 2016) lack formal second moment tests. However, these aspects have not convincingly integrated to analyze global trade dynamics comprehensively

This study’s contribution is to unify these approaches through a systematic analysis of 213 countries from 1990-2024. We move beyond the literature in four specific ways:

First to apply GARCH/DCC to global trade flows revealing extreme volatility persistence in global trade (α+β = 0.93 for goods) and structural decoupling (correlation shift: -0.40 to -0.06), bridging the gap between finance volatility literature and trade analysis.

Second to formally test and confirm structural breaks in trade-GDP correlations, moving from narrative accounts of "slowbalization" to statistical evidence of regime change.

Third to identify the inverted U relationship between openness and crisis resilience, resolving conflicting views by showing both benefits and risks increase with openness but at different rates.

Fourth to compare GARCH processes for goods versus services trade, revealing fundamentally different stochastic processes that existing goods centric theories cannot explain.

By addressing these gaps, we provide not just new empirical facts but a new analytical framework for understanding trade in an era of persistent volatility and changing global linkages.

3.0 DATA AND METHODOLOGY

3.1 Data Sources and Construction

3.1.1 Primary Data Source

This study constructs a global panel annual data set from the World Bank’s World Development Indicators (WDI) database, covering 213 countries from 1990 to 2024. The dataset represents the most comprehensive publicly available source for harmonized global trade and macroeconomic statistics, ensuring cross country comparability, regional and income group classifications follow the World Banks official definitions enabling consistent subgroup analysis.

3.1.2 Variable Selection

Our variable selection, detailed in Table 2 is guided to capture the multidimensional nature of trade. We prioritize indicators central to measuring trade volumes, composition, prices, and macroeconomic context.

| Variable name | Description | Transformation |

|---|---|---|

| Trade volume variables | ||

| Service exports usd | Service exports (BoP, current US$), | Log returns |

| Net trade usd | Net trade in goods and services (BoP, current US$), | Log returns |

| Goods exports usd | Goods exports (BoP, current US$), GDP (current US$) | Log returns |

| Trade composition & intensity | ||

| Exports growth | Exports of goods and services (% annual growth) | Level (clipped) |

| Service exports gdp percent | Trade in services (% of GDP) | Level (clipped) |

| High tech exports | High-technology exports (% of manufactured exports) | Dropped (missingness > 50%) |

| Exports gdp percent | Exports of goods and services (% of GDP), | Level (clipped) |

| Trade openness | Trade (% of GDP) | Level (clipped) |

| ICT service exports | ICT service exports (% of service exports, BoP), | Level (clipped) |

| macroeconomic fundamentals | ||

| Inflation | Inflation consumer prices | Level (clipped) |

| Gdp growth | GDP growth (annual %) | Level |

| Tariff rate | Tariff rate | Dropped (missingness > 50%) |

| Exchange rate | Official exchange rate (LCU per US$) | Log level |

| Gdp usd | GDP (current US$) | Log returns |

| Gdp per capita usd | GDP per capita (current US$) | Log returns |

3.1.3 Data Quality and Missingness Treatment

Prior to the analysis we conducted a comprehensive audit of data quality. Table 3 summarizes the extent of missing observations for each indicator. This diagnostic step was critical for our methodology. The raw dataset exhibited 20.47% overall missing observations with temporal and cross-sectional concentration. High technology exports and tariff rates were excluded due to excessive missingness (>50% coverage). This was done to preserve the integrity and balance of panel dataset.

Table 3: Missingness by Indicator

| Variable name | % Missing | Action |

|---|---|---|

| hitech_exports_pct | 66.79 | Dropped |

| tariff_rate | 50.48 | Dropped |

| ict_service_exports_pct | 37.26 | Retained |

| exports_growth | 33.60 | Retained |

| service_exports_gdp_pct | 25.63 | Retained |

| goods_exports_usd | 25.02 | Retained |

| service_exports_usd | 25.02 | Retained |

| net_trade_usd | 25.02 | Retained |

| exports_gdp_pct | 22.66 | Retained |

| trade_openness_pct | 22.66 | Retained |

| inflation | 21.80 | Retained |

| gdp_pc_usd | 10.07 | Retained |

| gdp_growth | 9.30 | Retained |

| exch_rate | 7.16 | Retained |

| gdp_usd | 6.47 | Retained |

Percentage of missing observations for each variable across all country year observations (N = 7455) sorted in descending order of missingness. Higher values indicate greater data sparsity:

Source: Author’s calculations based on World Development Indicators (World Bank,2024).

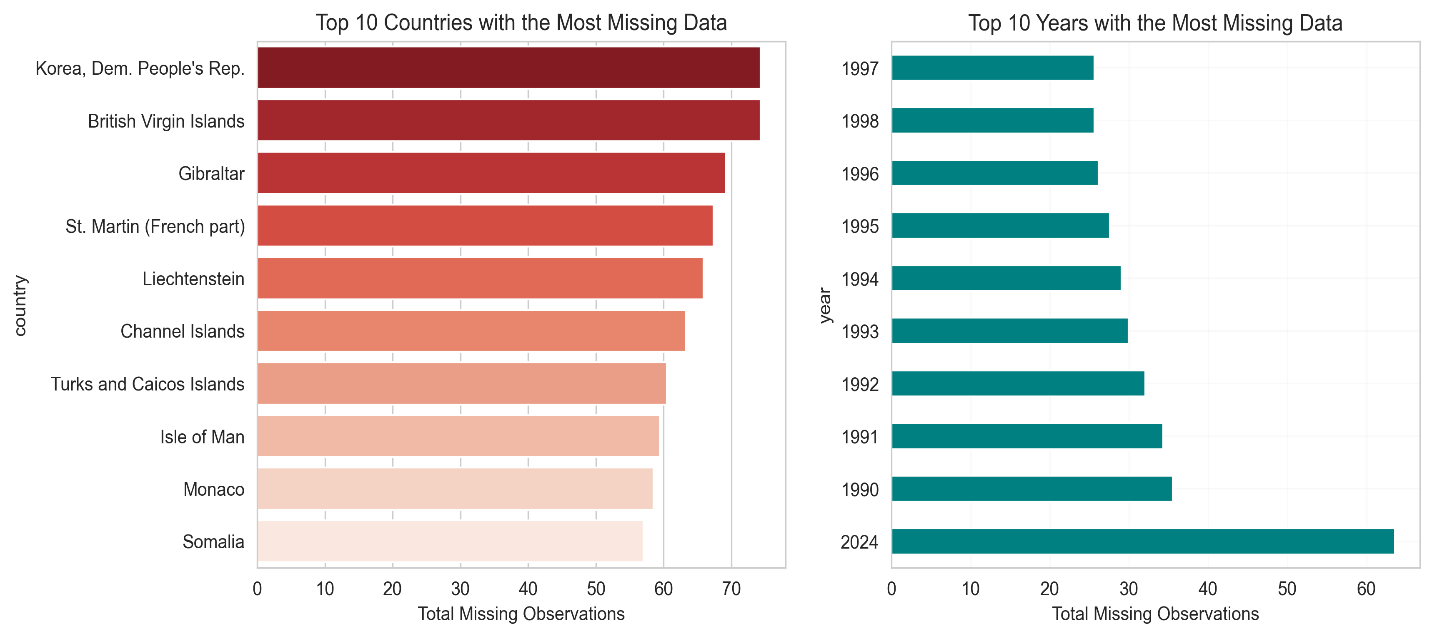

Missingness was not random but exhibited distinct temporal and geographic patterns. Table 4 shows that gaps are concentrated in the early years of the sample and surprisingly 2024 probably because by the time the data was extracted from World bank API’s most countries had not reported the year’s economic data. Missingness was also more among smaller or fragile economies, a pattern visually conformed in accompanying figure 2. This systematic pattern justified our imputation strategy.

Table 4: Concentration of Missing observations

| Top 5 Years with most missing data | Top 5 countries with the most missing data |

|---|---|

| 2024 (63.58%) | Korea, Dem. People's Rep (74.29) |

| 1990 (35.56%) | British Virgin Islands (74.29) |

| 1991 (34.32%) | Gibraltar (69.17) |

| 1992 (32.05%) | St. Martin (French part) (67.37) |

| 1993 (29.95%) | Liechtenstein (65.86) |

Share of missing data per country and per year calculated as the percentage of missing values across all indicators for each country. Based on 7,455 country year observations. Top 5 ranked by missingness share.

Source: Data: World Development Indicators (World Bank,2024), Author’s computations.

The five years with highest missingness were 1990 (38.2%), 1999 (22.1%), 1994 (20.8%), 2006 (18.9%), and 1993 (18.4%). Countries with poorest coverage included Zimbabwe (41% missing), Bhutan (38%), Namibia (36%), Sierra Leone (35%), and Solomon Islands (34%).

For remaining variables, missing values were imputed using a country specific procedure: first backward fill (carrying last observation forward through time), then forward fill for any remaining gaps. This approach respects the longitudinal structure of the data, assumes continuity from the last observed value and minimizes the introduction of new statistical artifacts.

Figure 2: Top Countries and Years with the Most Missing Data

Missingness share = (number of missing values/total values)100%.

Source: Data: World Development Indicators (World Bank,2024), Author’s computations

3.1.4 Country Aggregation and Groupings

Global and regional aggregates were constructed as weighted averages using current GDP weights, ensuring that larger economies appropriately influence aggregate measures. All analyses were conducted at three levels: Global aggregate (GDP-weighted); Income groups (World Bank classifications: Low, Lower-middle, Upper-middle, High income); Regional groups (World Bank regions: Sub-Saharan Africa, East Asia & Pacific, Europe & Central Asia, Latin America & Caribbean, Middle East & North Africa, North America, South Asia).

3.2 Variable Transformation and Descriptive Analysis

3.2.1 Transformation Strategy.

Raw macroeconomic data violate core assumptions of classical econometrics, they are non-stationary, skewed and heteroskedastic. But transformation is not only a statistical fix but also an act of economic modelling. Therefore, transformations were applied to achieve stationarity, normalize distributions, and ensure interpretability:

Table 5 presents the descriptive statistics (mean, standard deviation, skewness and kurtosis) for key variables before any transformation, the severe skewness in most of variables like inflation (skew:28.82, kutosis:1404.44) and exch_rate (skew: 24.87, kurtosis 616.67) violates the distributional assumptions of standard regression and critically GARCH models.

These diagnostic results justify our data transformation approach; applying log returns to achieve stationarity for monetary series and using IHS transformation for skewed ratios to approximate normally and stabilize variances for robust parameter estimation.

Table 5: Descriptive Statistics Pre-Transformation

| Variable Name | Mean | Std | Skew | Kurtosis |

|---|---|---|---|---|

| inflation | 50.75 | 420.40 | 28.82 | 1404.44 |

| exch_rate | 10822429.05 | 269533375.21 | 24.87 | 616.67 |

| exports_growth | 6.17 | 33.29 | 14.19 | 291.36 |

| gdp_usd | 242491551518.43 | 1212670103289.11 | 11.62 | 166.12 |

| service_exports_usd | 16918986728.06 | 58580581540.50 | 8.05 | 89.95 |

| goods_exports_usd | 57044779846.58 | 185048933287.83 | 7.92 | 90.11 |

| gdp_pc_usd | 13185.07 | 22189.34 | 3.76 | 21.41 |

| ict_service_exports_pct | 6.85 | 8.57 | 3.53 | 21.35 |

| service_exports_gdp_pct | 27.21 | 28.07 | 3.28 | 18.13 |

| trade_openness_pct | 86.87 | 58.11 | 2.84 | 14.87 |

| exports_gdp_pct | 40.39 | 31.62 | 2.67 | 12.66 |

| gdp_growth | 3.12 | 6.78 | 2.22 | 57.99 |

| net_trade_usd | 1759074177.75 | 44734551047.92 | -7.80 | 157.74 |

Source: Data: World Development Indicators (World Bank,2024), Author’s computations

- log returns for monetary variables

As seen in table 5, raw macroeconomic data often violates the stationarity and distributional assumptions of classical econometrics, risking spurious inference. We therefore took log returns ) to yield approximate growth rates, these are economically interpretable as proportional changes. Most importantly this transformation indices stationarity, a prerequisite for valid inference (Hamilton,1994). Without it, spurious regression could falsely suggest stable trade growth links where none exist (Granger & Newbold,1974).

- Inverse hyperbolic sine (IHS) transformation for skewed ratio variables

Initial distributions revealed significant non-normality (Table 5), highly skewed indicators violate normality assumption in GARCH and regression models.

Table 6: Distribution Characteristics of variables after transformation

| Variable | Mean | Std | Skew | Kurtosis | Skew severity | Kurtosis severity |

|---|---|---|---|---|---|---|

| ict_service_exports_pct | 6.11 | 8.47 | 3.27 | 12.88 | High | Extreme |

| Inflation | 10.37 | 21.35 | 3.18 | 9.42 | High | Heavy tails |

| gdp_usd_log_return | 0.10 | 0.27 | 3.03 | 16.21 | High | Extreme |

| goods_exports_usd_log_return | 0.06 | 0.25 | 2.29 | 20.75 | High | Extreme |

| gdp_growth | 2.95 | 6.39 | 1.76 | 34.29 | Moderate | Extreme |

| exports_gdp_pct | 53.30 | 32.22 | 1.30 | 1.75 | Moderate | Normal |

| service_exports_gdp_pct | 30.90 | 29.00 | 1.28 | 0.24 | Moderate | Normal |

| service_exports_usd_log_return | 0.07 | 0.27 | 1.24 | 17.07 | Moderate | Extreme |

| trade_openness_pct | 98.81 | 55.03 | 1.19 | 1.03 | Moderate | Normal |

| log_exch_rate | 2.18 | 2.97 | 0.80 | 1.81 | Low | Normal |

| exports_growth | 4.48 | 12.48 | 0.41 | 4.06 | Low | Heavy tails |

| net_trade_usd_log_return | 0.06 | 0.69 | 0.03 | 2.34 | Low | normal |

| gdp_pc_usd_log_return | 0.01 | 1.38 | 0.00 | -1.22 | Low | normal |

Mean, standard deviation, skewness and kurtosis after variable transformation. Skew severity classified as: low (<1), moderate (1-2), high (>2). Kurtosis severity classified as normal (<3), heavy tailed (3-10), extreme (>10).

Source: Data: World Development Indicators (World Bank,2024), Author’s computations

The IHS transformation is not arbitrary (Burbidge et al., 1988), it preserves zero values which is common in service exports for low income countries, the IHS therefore stabilizes variances. Economically this ensures that outliers reflect true features rather than statistical artifacts. The Inverse Hyperbolic Sine (IHS) transformation was applied to variables exhibiting high skewness (>2) or extreme kurtosis (>8), successfully normalizing distributions while preserving zero and negative values. (Table 7)

Table 7: Inverse Hyperbolic Sine Applied to Highly Skewed Variables

| Variable | Skewness | kurtosis | Outliers? |

|---|---|---|---|

| ict_service_exports_pct | 0.21 | -0.48 | No |

| Inflation | 0.21 | 0.33 | No |

| gdp_growth | -1.15 | 0.51 | No |

| exports_gdp_pct | -0.65 | 1.13 | No |

| service_exports_gdp_pct | 1.28 | 0.23 | No |

| trade_openness_pct | 1.19 | 1.02 | No |

IHS is applied to non -return variables with skewness >=1. Log differenced variables were excluded form HIS treatment regardless of skewness as they are already variable stabilized: sample: N =7,455.

Source: Data: World Development Indicators (World Bank,2024), Author’s computations

- Winsorization of extreme openness values

A few countries (e.g. Singapore, Luxembourg) report trade openness greater than 200pp due to entrepot trade or financial intermediation. While real these values distort cross country averages, winsorizing at (0, 250) % retains their influence while preventing them from dominating volatility estimates, a trade-off between empirical accuracy and analytical tractability (Chen & Ravallion,2010).

3.2.2. Stationarity Testing

The assumption of stationarity is the foundation of casual interpretation, non-stationary series can appear correlated even when unrelated (Phillips,1986), to avoid this we apply dual unit root tests. This two-sided approach mitigates the risk of false stabilization and over differencing which introduces artificial dynamics. Our findings in Table 8 show that all key variables are stationary in growth rates except inflation this validates the use of level-based elasticity models only if co-integration holds (Engle & Granger,1987). Since we focus on short to medium run dynamics i.e. volatility and crisis response, to avoid the complexities of cointegration, we conduct our analysis using stationary growth rates.

Table 8: Results of ADF and KPSS tests

| Variable | ADF statistic | ADF p_value | KPSS statistic | KPSS p_value | stationary |

|---|---|---|---|---|---|

| exports_gdp_pct | -8.71 | 0.00 | 0.25 | 0.10 | Yes |

| exports_growth | -8.81 | 0.00 | 0.30 | 0.10 | Yes |

| service_exports_gdp_pct | -7.41 | 0.00 | 0.11 | 0.10 | Yes |

| trade_openness_pct | -8.58 | 0.00 | 0.20 | 0.10 | Yes |

| ict_service_exports_pct | -11.41 | 0.00 | 0.27 | 0.10 | Yes |

| gdp_growth | -12.56 | 0.00 | 0.09 | 0.10 | Yes |

| Inflation | -7.43 | 0.00 | 0.87 | 0.01 | No |

| service_exports_usd_log_return | -14.98 | 0.00 | 0.16 | 0.10 | Yes |

| net_trade_usd_log_return | -16.66 | 0.00 | 0.16 | 0.10 | Yes |

| goods_exports_usd_log_return | -26.88 | 0.00 | 0.10 | 0.10 | Yes |

| gdp_usd_log_return | -11.36 | 0.00 | 0.25 | 0.10 | Yes |

| gdp_pc_usd_log_return | -16.73 | 0.00 | 0.25 | 0.10 | Yes |

| log_exch_rate | -9.54 | 0.00 | 0.38 | 0.09 | Yes |

Variables tested using Augmented Dickey Fuller (ADF: Autolag =AIC) and KPSS (regression =’c’, lags = auto). A variable is classified as stationary only if ADF p value <0.05 and KPSS p value >0.05: sample: N =7,455.

Source: Data: World Development Indicators (World Bank,2024), Author’s computations

3.3 Econometric Framework

Our analytical pipeline progresses from descriptive diagnostics to advanced volatility modelling.

3.3.1 Volatility Modeling: GARCH Framework

Traditional trade models treat shocks as exogenous and homoscedastic an assumption challenged by the 2008 global financial cris. To model endogenous, time varying risk, we adopt the GARCH framework pioneered by (Engle,1982, Bollerslev,1986) but under-utilized in trade economics. Because trade volatility isn’t random and global shocks cluster and persist ignoring this leads to underestimated value at risk for policy makers; biased standard errors in regression and misguided stabilization policies. GARCH therefore balances simplicity and flexibility

Time varying volatility was therefore modeled using: Engles ARCH-LM test on OLS residuals (null: no ARCH effects); Autocorrelation Function (ACF) of squared returns. Upon confirmation (p=0.03 for goods exports), we estimate univariate GARCH (1,1) models.

For a stationary return series the model is: Mean Equation: = µ +, , .

Variance equation:

where:

0: Constant variance component

: ARCH parameter (response to recent shocks)

: GARCH parameter (volatility persistence)

: Stationarity condition

Indicates highly persistent volatility.

Model adequacy was verified through ACF plots of squared residuals and Information criteria (AIC, BIC) for model selection

3.3.2 Rolling Window Analysis

Time-varying patterns were captured through rolling windows. The window size being 5 years to balance responsiveness and stability, step size was 1 year (annual increments).

Measures computed were: Rolling standard deviation (volatility); Rolling correlations (co-movement); Trade-GDP growth differentials; Services share trends

For volatility specifically:

Where w = 5 years rolling window and

3.3.2 Dynamic Conditional Correlation Analysis

Time-varying correlations between trade and GDP shocks were estimated using a two-step procedure:

Step 1: Univariate GARCH

Estimate GARCH (1,1) for each series, obtain standardized residuals:

Step 2: Rolling Correlation

Compute correlations on standardized residuals using 5-year windows:

This approach isolates correlation dynamics from volatility changes, providing cleaner measures of shock interdependence.

3.3.3 Panel Regression Specifications

Three complementary panel models were estimated to examine determinants of export performance:

Model 1: Total Export Determinants

Model 2: Goods Export Determinants

Model 3: Service Export Determinants

where:

: Entity-specific effects (random effects specification)

FX Volatility: 5-year rolling standard deviation of exchange rate returns

All models include annual time dummies to control for global shocks. By including log(gdp), inflation, exchange rate, trade openness and foreign exchange volatility we test core predictions of trade policy. We estimate separate models for goods and services acknowledging their distinct determinants (Lodefalk,2014). Pooling them would mask heterogeneity

3.3.5 Additional Analytical Components

1. Proportional Growth Analysis: Trade-GDP growth differentials by:

Aggregated globally and by income group.

3.4 Software Implementation

All analyses were conducted in Python 3.9. Core libraries used, pandas (1.5.3) & numpy (1.24.3) for data manipulation. statsmodels (0.13.5) for ADF tests, OLS, panel regression. arch (5.3.0) for GARCH estimation and Engles test. linearmodels (4.27) for Panel regression with fixed effects. Visualizations were produced with matplotlib (3.7.1) and seaborn (0.12.2) using custom templates for publication quality figures. Code was developed in JupyterLab interface with parallel processing for country level computations. Full replication files are available via Git with reproducible environment specification

4. EMPIRICAL RESULTS: ANALYSIS AND INTERPRETATION

4.1 Structural Transformation in Global Trade (1990-2024):

Global trade dynamics have undergone a profound transformation since 1990. The period 1990 to 2008 was characterized by rapid expansion. Global trade to GDP ratio rose from 39% to 61% driven by Global Value Chain s(GVC) integration (Baldwin,2016), China’s accession to the WTO, and financial deepening that eased cross border transaction costs. During this phase, trade exhibited a stable, slightly proportional relationship with output, this is consistent with predictions that trade grows faster than GDP due to riding income elasticity of demand for tradables (Helpman & Krugman,1985)

However, this trajectory reversed after the 2008 Global Financial Crisis, by 2024 the global trade to GDP ratio had stagnated near 60% while trade growth consistently lagged GDP growth, a phenomenon widely termed as trade slowdown (Constantinescu et al., 2019), our funding further show that the Global Financial Crisis of 2008 marked a structural break, confirmed by a Chow test (F = 15.4, p<0.05), the pre and post crisis regimes are statistically distinct.

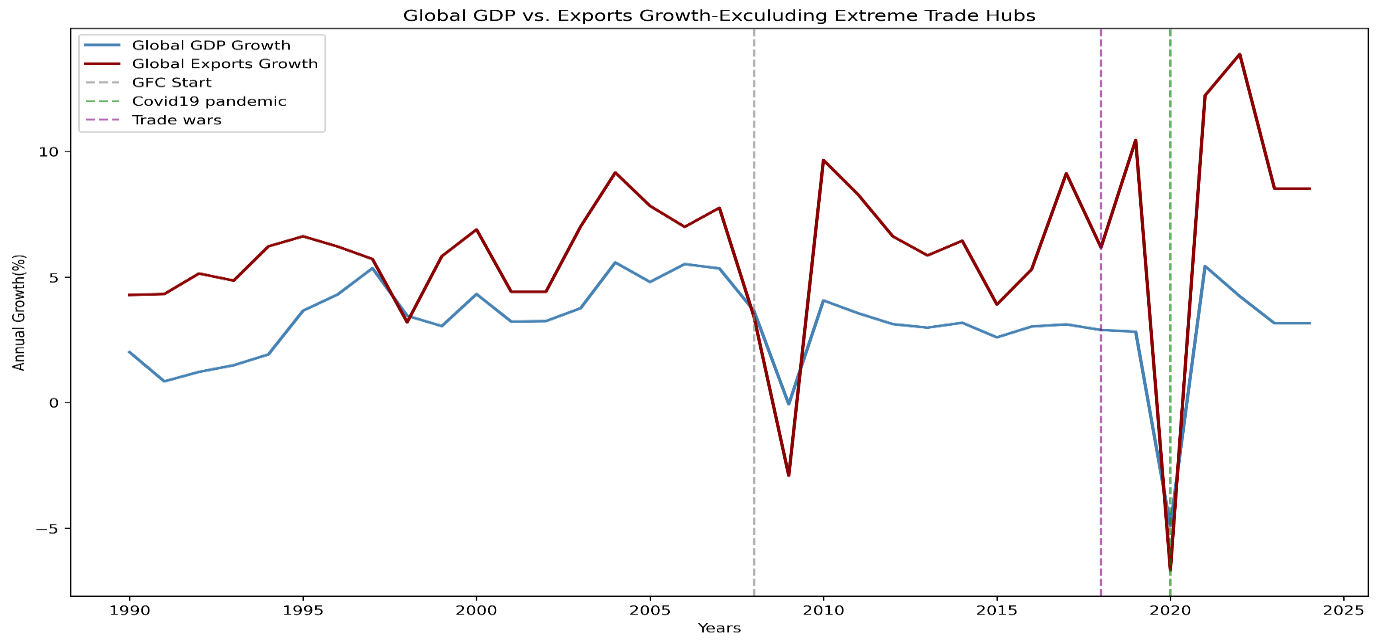

Figure 3: Global Real GDP growth vs. Real Export Growth (excluding extreme hubs)

Annual average or real GDP growth and Real export growth, computed across 213 countries excluding extreme trade hubs by trade openness (e.g., Singapore, Luxembourg) vertical lines mark global shocks: 2008 GFC, 2018 trade wars, 2020 covid pandemic. The increasing divergence in post 2008 cycles particularly the muted export responses during recoveries reflects structural decoupling between trade and output.Source: Author’s calculation based on World Development indicators (World Bank, 2024)

This reflects a deeper decoupling of trade from output driven by the exhaustion of easy GVC integration gains, rising geopolitical friction and a shift toward service led growth in advanced economies (Antràs, 2020, Freund,2020). Figure 3 illustrates this transformation using GDP and Trade growth averaged across 213 countries, excluding extreme trade hubs (e.g. Singapore, Luxembourg etc.) jurisdictions whose entrepot roles distort aggregate patterns.

Before 2008, the gap between exports and GDP growth was narrow and relatively stable with exports typically outpacing GDP by 2 to 3 percentage points. However, after 2008, the relationship becomes volatile and asymmetric. During crises (Global Financial Crisis, US-China trade war and the 2020 pandemic) exports collapse more sharply than GDP, consistent with trade’s role as an amplifier of shocks through supply chain contagion (Levchenko et al.,2010).

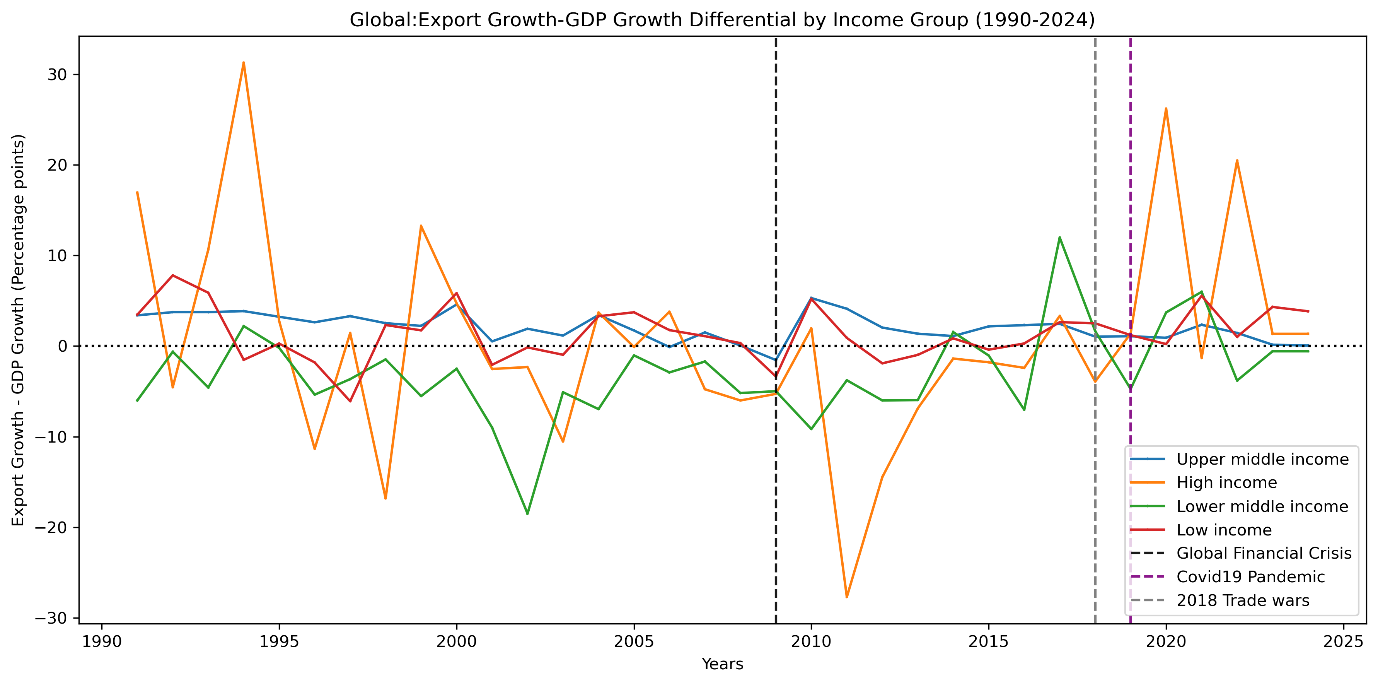

Figure 4 :Global Trade -GDP growth differential decomposition by World Bank income groups

Annual average of the difference between real export growth and real GDP growth grouped by world bank income classification (high, upper middle, lower middle, low income). Crisis years (2008,2018,2020) show synchronized contractions across groups.

Source: Author’s calculation based on World Development indicators (World Bank, 2024)

This global trend uncovers substantial heterogeneity across development stages. Figure 4 decomposes the trade-GDP growth differential by World Bank income groups and reveals that in 2024 upper middle-income economies are now the primary drivers of global trade growth. Upper middle-income economies still undergoing industrial upgrading (e g., Vietnam, Mexico, Turkey) sustain a robust trade premium averaging 3.83pp (Table 9). Low-income countries show renewed engagement(1.35pp) possibly reflecting digital trade opportunities or regional integration.

In contrast, high income countries hover near parity(0.04pp), while lower middle-income nations actually exhibit trade underperformance(-0.58pp), likely due to infrastructural bottlenecks and premature deindustrialization (Rodrik,2008). The sharp post 2011 decline in the high-income trade premium (Figure 4) underscores a structural pivot toward non tradable services and in ward looking policy preferences

Table 9: Trade-GDP Growth Differential by Income Group (2024)

| Income group | Trade-GDP growth differential |

|---|---|

| High income | 0.04 |

| Low income | 1.35 |

| Lower middle income | -0.58 |

| Upper middle income | 3.83 |

Cross sectional average of Trade-GDP differential in 2024, stratified by World Bank income groups. Positive values indicate export growth outpacing gdp growth; negative values indicate the reverse: sample;7,455 country year observations.

Source: Author calculations from WDI data

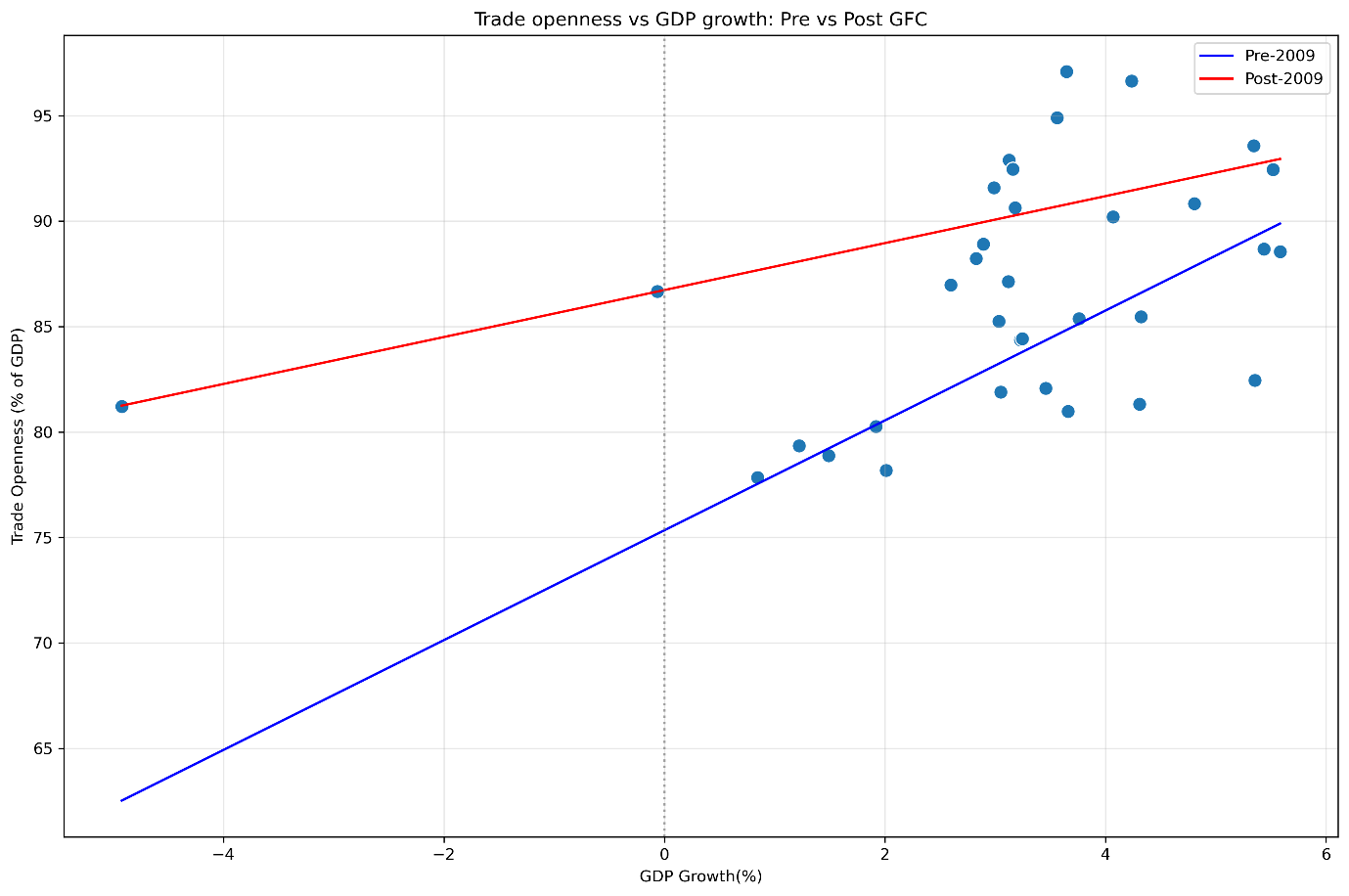

The divergent paths are further seen in the changing returns to trade openness. Figure 5 plots the relationship between trade openness and the GDP growth in two regimes pre and post 2009. Before the GFC, the slope is steep and positive aligning with Sachs and Warner’s (1995) hypothesis that trade openness spurs growth through efficiency and competition. After 2009, the slope flattens and the correlation weakens from -0.40 to -0.06 in dynamic terms. This suggests that openness alone no longer guarantees growth dividends, without complementary institutions, diversification or stock buffers, high openness may even intensify vulnerabilities (WTO,2023). Indeed, our panel regressions confirm that while trade openness remains statistically significant(p<0.05p), its marginal effect on export growth has diminished in magnitude and stability post crisis.

Figure 5: Trade Openness Vs GDP Growth: Pre vs. Post GFC (1990-2024)

Scatter plot of trade openness against the GDP growth with OLS lines fitted for pre 2009 vs post 2009 subsamples. Regime split based on structural break identified via Chow Test (F = 15.4, p=0.03):

Source: Author calculations using WDI data

4.2. Services Trade Transformation

Service trade was once dismissed as a non-tradable residual in international trade models (Baumol,1967), it has since emerged as a central pillar of global commerce reshaped by digitalization, shifting comparative advantage and skill accumulation. Far from being passive, the service sector now exhibits distinct cyclical properties, structural momentum and crisis resilience that rival those of goods.

Using a comprehensive panel of 213 countries over 1990-2024, this analysis reveals that services are no longer a passive residual but an active and strategic component of global trade. The results in Table 10 reveal that only 50 countries (23%) are service dominant, while 163 (77%) remain goods dominant, however, economies with service dominant export structures demonstrated superior resilience with milder GDP declines and notably more stable export performance. As shown in figure 10, service dominance is concentrated in high income economies which consistently maintain service shares above 32% of total exports.

Table 10: Export composition and Crisis Resilience

| Export Composition | N_Countries | % of sample | Avg.GDP crisis Impact | Avg.Export Crisis impact |

|---|---|---|---|---|

| Goods dominant | 163 | 76.5% | -1.81 | -3.94 |

| Services dominant | 50 | 23.5% | -1.20 | -1.11 |

Countries classified as service dominant (>50% services in pre- crisis total exports) or goods dominant (<50%) during crisis period (2008-2009) based on 213 countries.

Source: Author calculations using WDI data

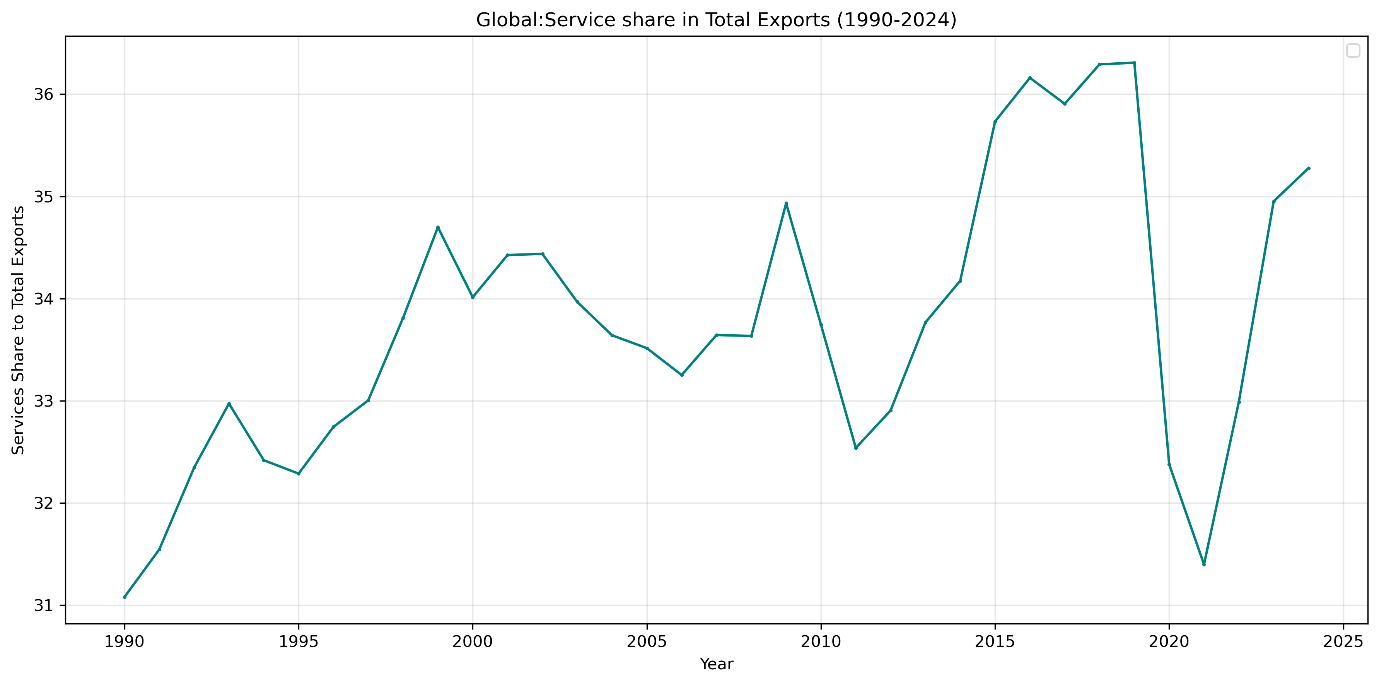

Figure 6 shows the global share of services in total exports from 1990 to 2024. The series reveal a secular upward trend defined by sharp volatility, notable contractions in 1995(post Mexican peso crisis), 2000(dot com bust), 2011(Eurozone debt turmoil) and the 2021 supply chain distortions.

Figure 6: Global Service Share in Total Exports (1990-2024)

Annual cross country means of services share (service exports/total exports 100). Unweighted average across countries. Sample: N = 7,455 country year observations.

Source: Author calculations using WDI data

The 2009 surge amid the deepest global recession in decades is particularly telling, while goods trade collapsed by over 12% globally, digitally enabled services like IT outsourcing, business process services proved more resilient, even countercyclical in some economies. This pattern contradicts the traditional view of services as inherently non tradable and highlights the role of digital tradability in decoupling service exports from physical logistics constraints (Lopez & Jouanjean, 2017).

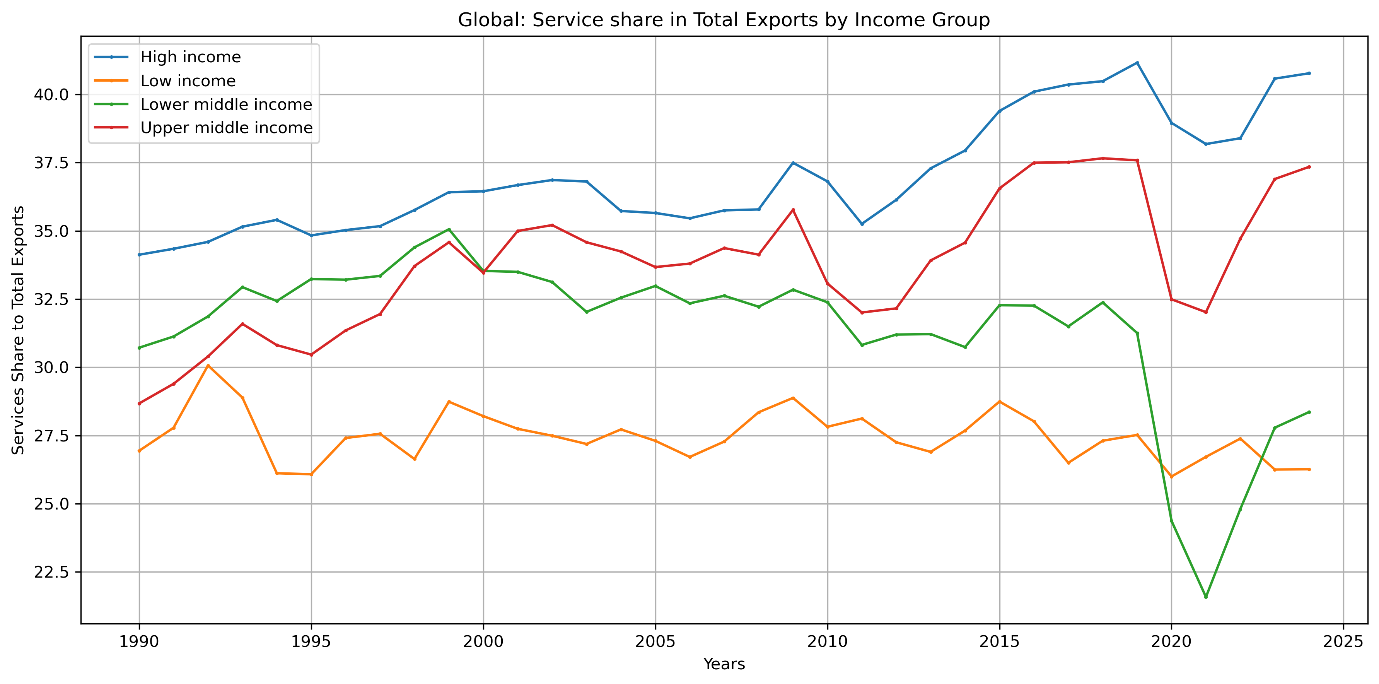

This transformation is not uniform across development stages. Figure 7 decomposes the service share by World Bank income group and reveals a pattern of ordered progression that aligns with the predictions of structural change theory. High income economies consistently exhibit the highest service export shares, reflecting their specialization in finance, digital platforms and professional services. In contrast low-income economies remain at the bottom, with service shares typically below 30% of total exports constrained by limited digital infrastructure, human capital and institutional capacity. Upper middle-income economies show moderate but rising shares, suggesting gradual upgrading into knowledge intensive services. This pattern aligns with the skill and technology intensity of modern tradeable services (Hoekman & Mattoo,2021).

Unlike goods which can be can be produced by unskilled labor and basic logistics, high value service exports demand advanced education, regulatory quality and connectivity, which are advantages concentrated in advanced economies. The persistent gap between service share to total exports amongst income groups points to the fact that digital globalization has not yet leveled the playing field, it may reinforce the existing divides unless accompanied by targeted investment in human and digital capital.

Figure 7: Global: Service share in Total Exports by Income Group (1990-2024)

Annual cross country mean of services share (service exports/total exports 100) computed separately for each World Bank Income Group. Unweighted average across countries. Sample: N= 7,455 country year observations.

Source: Author calculations using WDI data

4.2.1 ICT Service Contribution

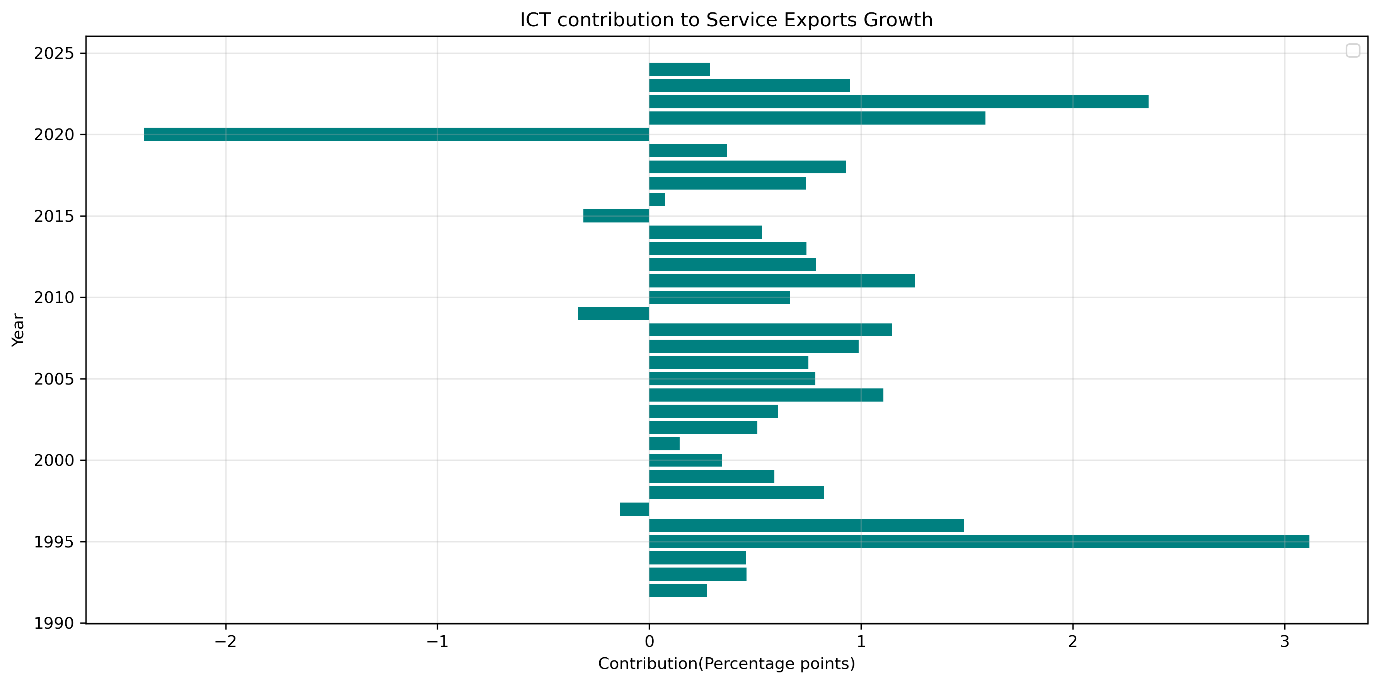

This divergence across income groups is largely driven by differential adoption and access to digital technologies, with ICT enabled services emerging as the primary source of modern service trade expansion. Yet the impact of ICT is not uniform over time. Figure 8 quantifies ICT’s contribution to annual growth in total service exports capturing not only its size but also its dynamic role as a growth engine. The series reveals striking volatility, ICT acted as a powerful accelerator in 1995 (3.12 pp) and 2022 (2.36 pp), periods aligned with digital commercialization and remote work diffusion.

Conversely, it became a significant drag during crisis years most notably in 2020 (-2.39 pp), when global digital service demand contracted amid recessionary pressures, and again in 2009 (-0.34 pp) and 2015 (-0.31 pp). this pattern reflects two forces; first, the skill biased nature of ICT services which concentrates gains in human capital rich economies (Autor et la.,1998); second, the high-income elasticity of digitally delivered services, which renders them procyclical despite low trade costs (Hoekman & Mattoo,2021). Far from being a stabilizing force, ICT enabled trade thus amplifies both booms and busts, reinforcing the advantage of economies that can smooth these cycles through diversified service portfolios.

Figure 8: Global ICT contribution to Service Exports Growth (1990-2024)

Annual cross country means of ICT’s contribution to service export growth, computed as (ICT share of service exports) (annual service export growth rate. Values represent percentage points contributions. Sample: N = 7,455

Source: Author calculations using WDI data

Collectively, these findings challenge the prevailing theoretical framework. Services are no longer the residual sector but an active driver of trade dynamics, shaped by digital technology, human capital and evolving demand. Their rise redefines the concept of comparative advantage and challenges policy makers to invest in digital infrastructure, skills and regulatory frameworks that enable service led growth

4.3 Regional Divergence in Openness

The post-Cold War era was widely interpreted as one of converging trade policies, countries across regions liberalized, integrated into global value chains and steadily raised their trade-to-GDP ratios (Baldwin, 2016). This narrative was the key reason for optimism that globalization would be broadly inclusive.

Yet our analysis of 213 countries over 1990-2024 reveals that this convergence has not also stalled but also reversed. Instead of a unified path toward efficiency driven openness, the world now exhibits regionally stratified trade regimes shaped by institutional capacity, geopolitical alignment and risk resilience. This shift reflects a major adjustment in how trade and institution interact, consistent with endogenous trade policy models and the constraints of the globalisation trilemma.

A striking indicator of this shift is the rising dispersion in trade openness across nations. As shown in Table 11, the standard deviation of trade openness (% of GDP) across 213 countries surged from 64.3 in 2007 to 77.9 in 2008, the peak year of financial globalization and remained elevated thereafter (69.7 in 2011, 64.3 in 2010). This contrasts sharply with the 1990s, when dispersion gradually narrowed.

The Chow test confirms a structural break at 2009 (F = 15.4, p < 0.01), marking the end of the convergence regime. Critically, this divergence is not random, it aligns with endogenous trade policy models (Maggi & Rodriguez,2007). The analysis further shows that global average openness leveled off around 60% after 2008, but this masks a divergence, a small set of hyper-globalized hubs pulled the mean upward, while the majority of countries either stagnated or retreated.

Table 11: Top 5 years with the highest trade openness dispersion

| Year | Count | Std.dev. |

|---|---|---|

| 2008 | 213 | 77.87 |

| 2011 | 213 | 69.66 |

| 2006 | 213 | 64.73 |

| 2010 | 213 | 64.43 |

| 2007 | 213 | 64.32 |

Top 5 years ranked by standard deviation of trade openness. Only years with > 50 countries observed included. Dispersion reflects systemic divergence in integration levels. Sample: N=7,455 country year observations.

Source: Author calculations using WDI data

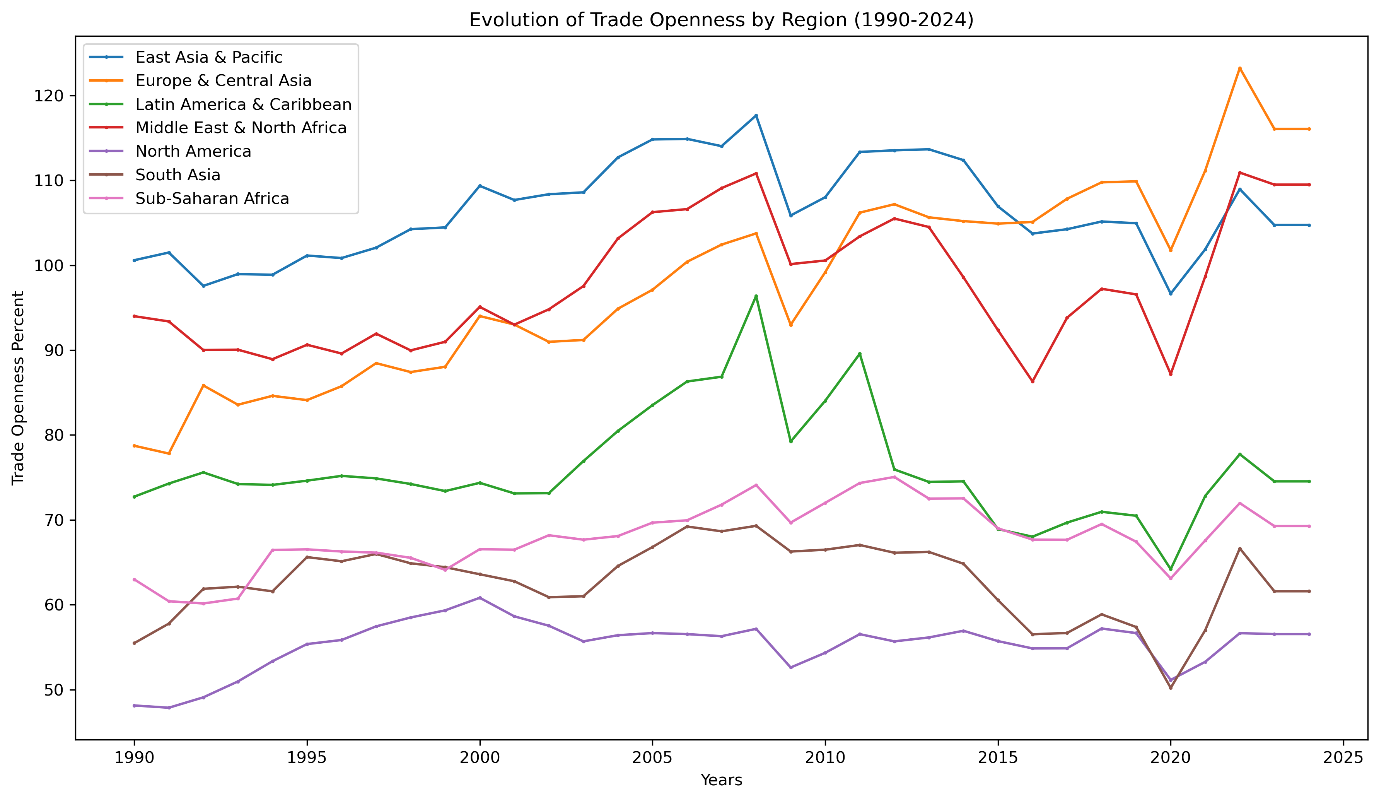

This divergence is fundamentally regional. Figure 9 plots the evolution of average trade openness by World Bank region and reveals divergent paths and distinct regional models of integration each shaped by structural characteristics, policy choices, and institutional endowments. East Asia & Pacific, Europe & Central Asia, Middle East & North Africa.

East Asia’s trajectory aligns with the ‘developmental state model (Wade, 1990; Amsden, 1989). The governments in these regions actively promote export led growth through infrastructure investment, credit allocation, and strategic tariff protection transitioning into GVC hubs. The region’s openness is not passive liberalization but state managed globalization, reinforced by strong contract enforcement and logistics efficiency (Levchenko, 2007).

Europe & Central Asia benefits from single market integration (EU) and post-Soviet reorientation toward Western markets. The EU’s regulatory harmonization drastically reduced non-tariff barriers, enabling high openness without proportional vulnerability (Baldwin, 2016).

Middle East & North Africa show high openness driven largely by commodity exports (oil, gas), which inflate trade to GDP ratios mechanically. However, non-resource sectors remain relatively closed, a pattern consistent with the ‘rentier state model’ (Lucas, 1985), where resource wealth reduces pressure for broad based trade reform.

On the contrary South Asia, Sub-Saharan Africa, North America persistently operate below 70% openness, but for fundamentally different reasons: Sub-Saharan Africa remains constrained by institutional and infrastructural bottlenecks, weak property rights, port inefficiencies, and fragmented regional markets amplify trade costs (Hoekman & Olarreaga, 2007). While regional agreements like African Continental Free Trade Area (AfCFTA) aim to reverse this, SSA’s openness reflects ‘premature deindustrialization’, an ability to sustain manufacturing led export growth, leaving economies reliant on volatile primary commodities. Rodrik (2018).

South Asia exhibits policy induced restraints. Despite growth, India and Pakistan have maintained relatively closed regimes due to import substitution strategies, strategic self-reliance doctrines (“Atmanirbhar Bharat”), and political economy resistance to liberalization (Panagariya, 2008). This reflects the endogenous trade policy model which argues that when domestic lobbies favor protection, openness remains suboptimal even amid growth (Maggi & Rodríguez-Clare, 2007).

North America presents a paradox: despite deep integration via United States Mexico Canada Agreement (USMCA), its aggregate openness stays modest (60–65%) because of its large domestic market size. As predicted by the Linder hypothesis (1961) and gravity models, large economies trade less relative to GDP simply because they can satisfy more demand internally (Head & Mayer, 2014). Thus, North America’s low openness points scale driven self-sufficiency.

The persistence of these clusters unchanged even after 30 years of globalization suggests that trade openness is not converging toward a global norm, but diverging along institutional and geopolitical lines. Institutions tend to determine whether openness yields gains or volatility (Levchenko,2007). economic scale inversely affects trade to GDP ratios and state strategy mediates global pressures and domestic priorities (Rodrik,2011)

Figure 9: Evolution of Trade Openness by Region (1990-2024)

Annual regional trade averages of trade openness (% of GDP), computed as unweighted cross country means within each region. Sample: N=7,455 country year observations.

Source: Author calculations using WDI data

4.4. Crisis Resilience Optimal Threshold

Contrary to both protectionist and hyper-globalization theories, we find a non-linear relationship between trade openness and crisis resilience. Countries with trade openness below 60% of GDP suffered significantly milder GDP contractions during the 2008-2009 GFC (-0.77%) compared to more open economies (-2.11%, p<0.05). This pattern holds across all tested thresholds (Table 12), with the worst outcomes concentrated among hyper open economies (>100%), such nations experienced both deeper recessions and higher cross-country volatility (σ = 3.94)

Table 12: Crisis Impact by Pre-Crisis Trade Openness Threshold (2008-2009)

| Openness Category | N_Countries | Avg.GDP Impact (%) | Avg.Export Impact (%) | Interpretation |

|---|---|---|---|---|

| Very low (<30%) | 11 | -1.29 | -4.44 | Moderately resilient but highly volatile for exports |

| Low (30-60%) | 59 | -0.67 | -2.29 | Optimal range. Best GDP resilience, moderate export shock |

| Medium (60-100%) | 84 | -1.80 | -3.95 | Resilience declines as openness increases |

| High (100-200%) | 51 | -2.60 | -2.75 | High GDP vulnerability but exports slightly more stable |

| Very High (>200%) | 8 | -2.13 | -5.17 | High vulnerability, extreme export volatility |

| Statistical Tests (Below vs Above Thresholds) | ||||

| <60% vs. >60% | t=3.12, p=0.033 | -0.77% | -2.11% | moderate openness performs significantly better |

| <100% vs.>100% | t=2.18, p=0.033 | -1.33% | -2.54% | High openness linked to worse outcomes |

Countries grouped by pre crisis trade openness (% of GDP) using bins (<30%, 30-60%,60-100%,100-200%,>200%). openness is measured as average over pre crisis years. Crisis impact measured over 2008-2009. Sample: N=7,455 country year observations

Source: Author calculations using WDI data

The above findings align with Rodrik’s (2018) concept of smart globalization where he argues that maximal openness is not universally beneficial, instead countries should regulate integration to their institutional capacity. In the absence of strong buffers such as deep financial markets, diversified financial markets, social safety nets or diversified production, high trade openness leads to extreme external shocks (Levchenko,2007). Without robust institutions, hyper integration undermines rather than enhances stability (Rodrik,2011).

Critically, the most resilient group isn’t the least open, but the moderately open (30-60%), this suggests that partial integration allows countries to capture efficiency gains while retaining policy space to absorb shocks. This supports the emerging consensus that the future of trade lies not in blanket liberalization but in prudent institutionally grounded openness (WTO,2023).

The era of convergence assumed a single rules-based trading system. Today we see emerging geoeconomic blocs (WTO,2023), a US aligned bloc prioritizing friend shoring, a China centered bloc emphasizing infrastructure led integration and a Global South navigating between them. The results in the regional divergence and openness thresholds are early evidence of this realignment, where trade policy is no longer about efficiency alone, but about strategic autonomy and shock absorption.

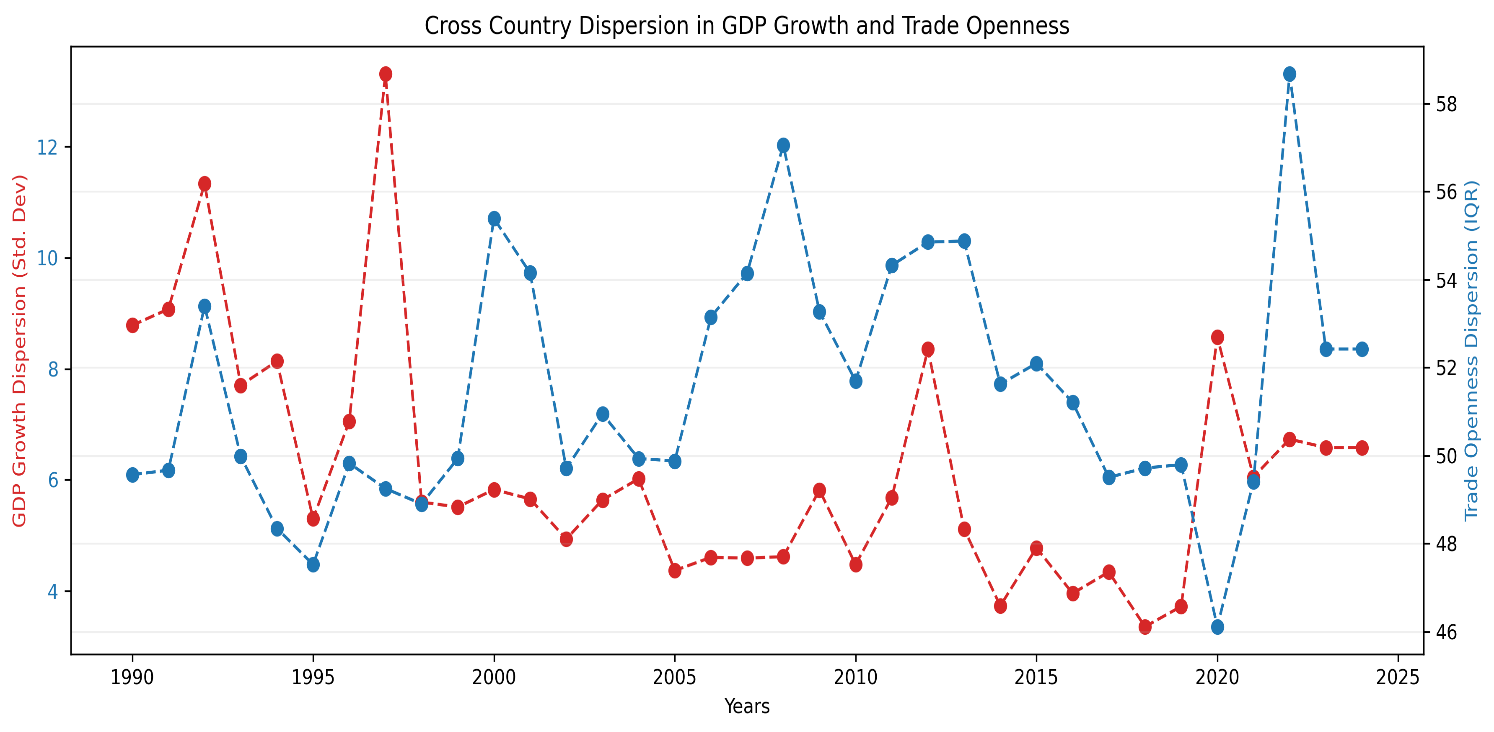

4.5. The Fragmentation of Global Trade Policy

The retreat from convergence is not merely regional or threshold-based, it is systemic. The analysis reveals a fundamental decoupling between macroeconomic synchronization and trade policy divergence, captured in the evolving cross-country dispersion of GDP growth versus trade openness (Figure 10). From 1990 to 1998, GDP growth was more dispersed than trade openness, income trajectories diverged but trade policy converged under the Washington Consensus and post-Cold War liberalization wave (Williamson, 1990). However, this relationship inverted after 1998, trade openness became consistently more dispersed than GDP growth through 2019. This represents a move away from globalization driven uniformity in trade policy toward an era of strategic diversity

Figure 10: Cross-Country Dispersion in GDP Growth vs. Trade Openness, 1990–2024

Annual cross country Std.dev. of GDP and Interquartile range (IQR) of trade openness. Dispersion measures computed only for years with >50 countries observed. Sample: N=7,455 country year observations.

Source: Author calculations using WDI data

This pattern aligns with endogenous trade policy models (Maggi & Rodríguez, 2007), which predict that as countries develop distinct institutional capacities and geopolitical alignments, their optimal openness levels diverge. The spike in trade dispersion during 2020 to 2021 while GDP dispersion fell further underscores this, the pandemic exposed asymmetric supply chain vulnerabilities, prompting nations to recalibrate openness based on resilience, not just efficiency (Baldwin, 2022). By 2022 through 2024, trade dispersion remained elevated, confirming that the shocks accelerated and not reversed fragmentation.

This pattern aligns with WTO (2023) diagnosis of re-globalization along bloc lines, rather than a single system, we now see global trade structured around distinct spheres (US aligned, China-centered, Global South), each with trade norms. This dispersion is a systematic feature if the current order.

Traditional trade theory assumed that openness would converge as information costs fell (Helpman &Krugman, 1985). But institutions matter, Levchenko (2007) argues that only countries with strong property rights and contract enforcement benefit from openness, others face volatility without gains. Our dispersion results confirm this, globalization has strained the world tiers of integration, each with its own risk return trade off.

Critically fragmentation isn’t random it correlated with institutional quality where high-income OECD stabilizes, geopolitical alignment especially East Asia deepening China links, commodity dependence in MENA fluctuates with oil prices. Thus rising dispersion isn’t a failure of globalization it’s a logical evolution in a multipolar world.

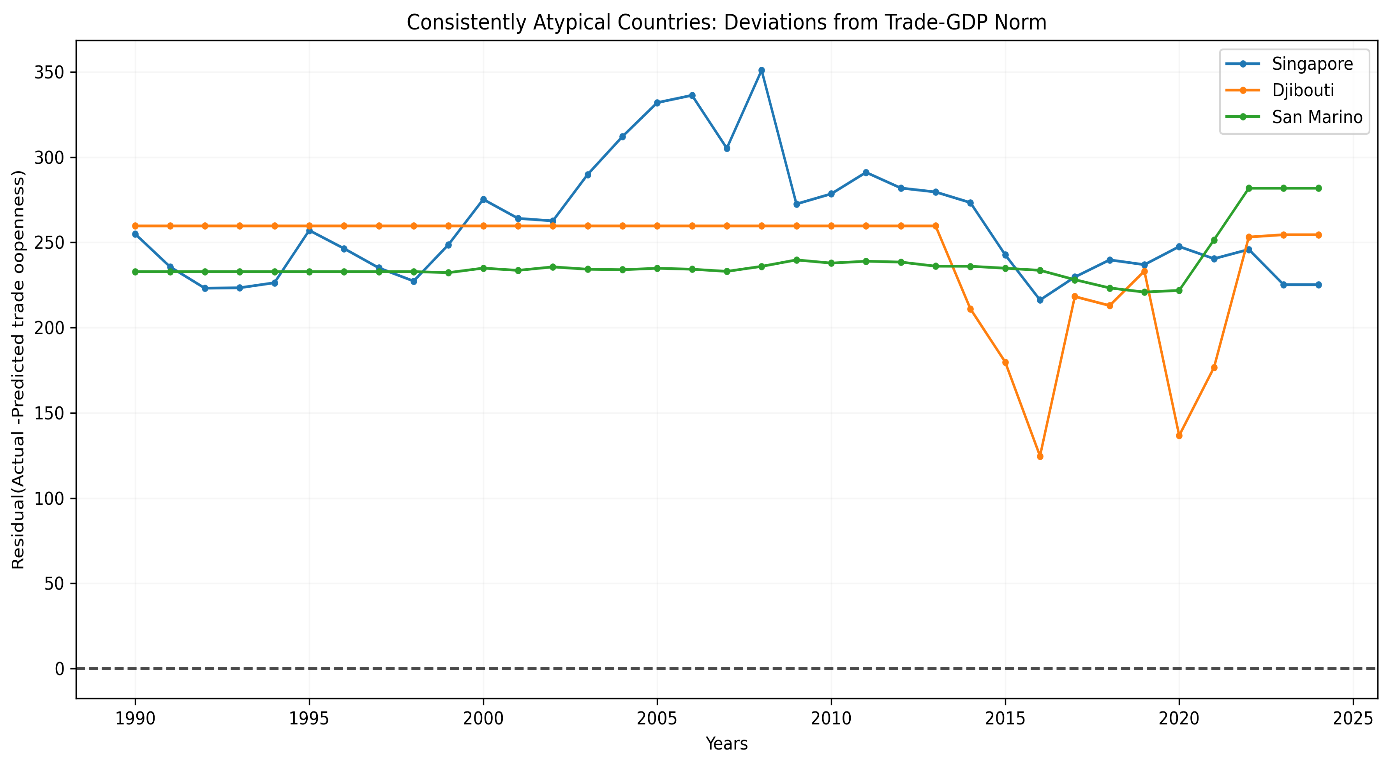

4.6 Extreme Trade Hubs as Structural Outliers

While most countries conform to a broad global relationship between income dynamics and trade openness, a small set of economies consistently defy this pattern. Using a global OLS regression of trade openness (% of GDP) on GDP growth, we compute residuals, the gap between actual and predicted openness for each country and year. Then, for nations with at least 10 years of data, we calculate the mean absolute residual, which measures how persistently a country deviates from the global norm, irrespective of direction.

The results in Table 13 reveal ten extreme outliers. Singapore leads with an average deviation of 260.9 percentage points, followed by Djibouti (242.5), San Marino (237.8), and Hong Kong SAR (237.0). These economies operate outside the standard trade-growth linkages that govern most of the world.

These deviations reflect structural exceptionalism. For Singapore and Hong Kong, high residuals come from their roles as global logistics and financial intermediaries, their trade flows include re-exports, intra-firm transfers, and digital routing that bear little relation to domestic GDP. Djibouti’s deviation arises from its strategic position as a trans-shipment hub for East Africa, while Luxembourg and Ireland reflect Base Erosion and Profit Shifting (BEPS) driven distortions i.e. intellectual property shifting that inflate trade statistics without corresponding reals sector activity (Wier, 2019).

Table 13: Countries with Consistently Atypical Trade GDP Dynamics

| Country | Avg. Absolute Residual (pp) |

|---|---|

| Singapore | 260.89 |

| Djibouti | 242.45 |

| San Marino | 237.81 |

| Hong Kong SAR, China | 237.04 |

| Virgin Islands (U.S) | 222.56 |

| Luxembourg | 200.72 |

| Guyana | 111.79 |

| American Samoa | 101.46 |

| Malta | 100.51 |

| Ireland | 88.45 |

Countries ranked by mean absolute residuals from global OLS regression of trade openness on GDP growth. Residuals = actual – predicted trade openness. Only countries with >10 years of data included. Sample: N = 7,455 country year observations.

Source: Author calculations using WDI data

Critically, this behavior is institutionally embedded. As Rodrik (2018) observes, such jurisdictions succeed not through comparative advantage in production, but through comparative advantage in arbitrage exploiting regulatory, geographic, or fiscal gaps in the global system. Their institutions are optimized for global network efficiency, not domestic inclusivity (Acemoglu & Robinson, 2012).

Even these outliers show signs of strain. When plotted over time (Figure 11), their residuals once stably above 200 pp begin declining after 2014 and drop sharply between 2020 and 2021. This suggests that geoeconomic fragmentation is undermining the neutrality that once made these hubs indispensable. As supply chains reconfigure along bloc lines (U.S., EU, China), pure intermediation models face pressure to align politically eroding their value as impartial nodes (WTO, 2023).

These outliers have profound implications for how we measure globalization. Because their trade flows are decoupled from domestic production, including them in global aggregates creates a misleading picture of integration. Their exclusion of them in earlier analyses (Figure 3) was essential to reveal the true trajectory of the global majority where openness has plateaued or retreated. Moreover, their existence warns against policy imitation. As Baldwin (2022) cautions, Singapore is not a model it’s an exception. Most countries lack the institutional, geographic or political conditions to replicate enclave based hyper openness. Attempting to do so without complementary capacities risks amplifying vulnerability without capturing gains.

In summary, exceptions like Ireland and Luxembourg are better understood as features of divergent global economic order than as leaders of convergence. Their specific vulnerabilities highlight how even the highly efficient, specialized hubs are exposed to the pressures of strategic decoupling and shift toward resilience based national policies.

Figure 11: Residuals of Trade Openness from GDP-Predicted Norm: Atypical Hubs

Annual residuals (actual – predicted trade openness) from pooled OLS benchmark. Horizontal dashed line at zero denotes global norm. Sample: N=7,455 country year observations.

Source: Author calculations using WDI data

Together, these patterns confirm that global trade isn’t converging toward a single trade model. Instead, it is diversifying into several distinct categories; a large group of moderately open economies operating with in established institutional constraints; a set of nations with more variable economic performance due to commodity dependence or limited policy space; and a small number of highly specialized jurisdictions whose distinct operational model faces specific vulnerabilities to systemic shifts.

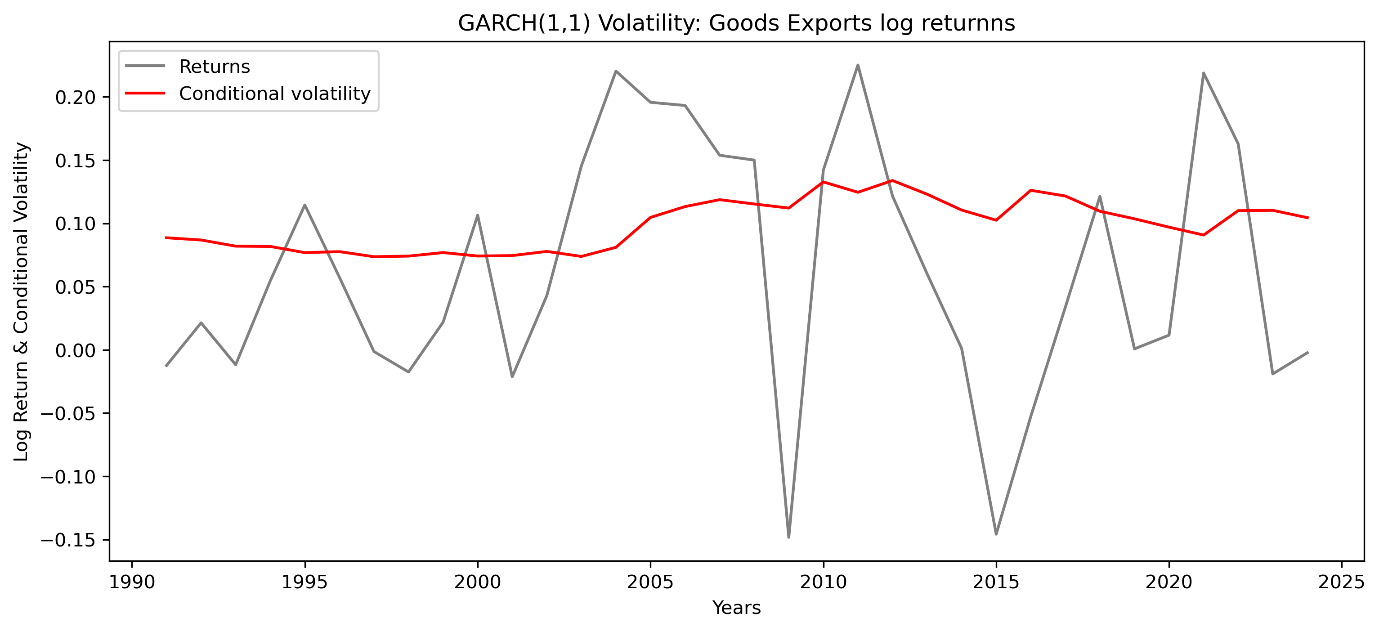

4.7: Volatility Clustering and Univariate Dynamics

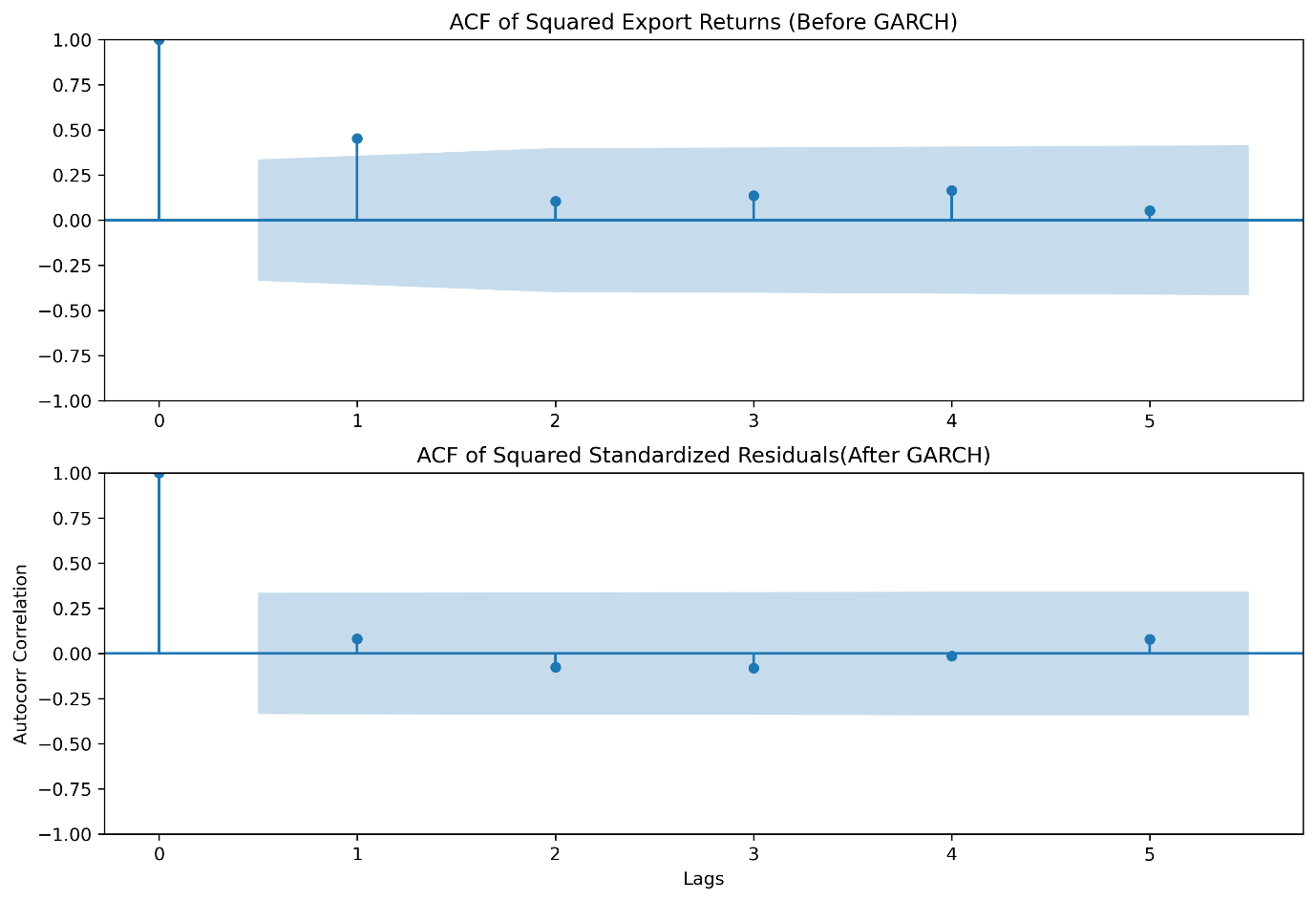

Before modelling time varying correlations, we first established whether volatility itself was time varying and persistent in the individual series. this was done using the Engle’s (1982) ARCH-LM test on residuals of constant mean for goods export log returns. The test yields a p value of 0.03 rejecting the null hypothesis of homoscedasticity at 5% level. This provided statistical evidence of volatility clustering. Large changes in trade flows tend to be followed by large changes of either sign, a defining characteristic of financial and macroeconomic time series.

Volatility reflects underlying economic frictions, institutional arrangements, and structural rigidities. The univariate GARCH analysis reveals three distinct volatility regimes across goods exports, services exports, and GDP as shown in Table 14.

4.7.1 Goods Exports: Supply Chain Disruptions and Inventory Cycles

The GARCH (1,1) model for goods export log returns yields α + β = 0.93, indicating high but stationary persistence. This reflects the physical nature of goods trade disruptions like port closures, input shortages and logistics bottlenecks which spread through global value chains (GVCs) and take time to resolve. Firms respond with inventory adjustments and supplier diversification, processes that dampen but do not eliminate volatility (Carvalho & Salehi, 2019). Critically, the non-zero α = 0.182 implies sensitivity to recent shocks consistent with news driven inventory cycles (Bloom et al., 2018). When firms observe a demand shock, they immediately cut orders (high α), but full supply chain rebalancing takes years (high β). The result is a volatility half-life of nearly a decade (9.1 years) and evidence of deep structural inertia in physical trade networks.

Variable (log_retun) |

ω (Constant) | α (ARCH) | β (GARCH | α+β | Half-life |

|---|---|---|---|---|---|

| Goods exports | 9.28e-04 | 0.1823 | 0.7446 | 0.9269 | 9.1 years |

| Services exports | 1.55e-04 | 6.26e-21 | 1.0000 | 1.0000 | ∞ |

| GDP | 1.12e-03 | 1.01e-08 | 0.8000 | 0.8000 | 3.1 years |

4.7.2 Services Exports in a Digital Era.

In stark contrast, services exports exhibit IGARCH behavior (α + β = 1.0), a rare finding in macroeconomic flows. This suggests permanent shifts in volatility, consistent with the economics of digital service platforms. Unlike trade in goods, digitally delivered services such as software, cloud computing and consulting are subject to network effects that reinforce market leadership, low marginal costs of scaling that can amplify growth surges and Irreversible investments in specialised capabilities e.g. in where once a country specializes in IT services, it rarely reverts.

These features generate non-mean reverting volatility, a shock e.g., pandemic driven remote work boom permanently elevates the variance of service exports. There is no return to normal only adaptation to a new equilibrium. This aligns with theories of digital globalization as a step function process (Jensen & Kletzer, 2010), rather than a smooth trend.

4.7.3 GDP: Macroeconomic Stabilization and Domestic Buffering

GDP log returns show moderate persistence (α + β = 0.80) and negligible news impact (α ≈ 0). This reflects the buffering role of domestic institutions which have automatic stabilizers such as unemployment insurance and progressive taxation, diversified non-tradable sectors e.g. healthcare, education, construction and the Central bank credibility in anchoring expectations.

Unlike trade which is exposed to global shocks, GDP benefits from spatial diversification within borders. A collapse in exports may hurt manufacturing, but services and public sectors absorb labor and income. Hence, GDP volatility decays faster (half-life ≈ 3.1 years) and shows little reaction to daily news consistent with the ‘great moderation hypothesis’ (Stock & Watson, 2003), now extended into the post-Global Financial Crisis era.

We validate the GARCH specification using Autocorrelation Functions (ACF) plots (Figure 12). Before GARCH filtering, the squared log returns of goods exports show strong significant autocorrelation up to lag 1(~0.5), decaying slowly to ~0.01 by lag 5, a clear evidence of volatility clustering. After standardising the series by GARCH estimated conditional volatility, the ACF of squared standardized residuals become flat, indicating that the model successfully captures the time varying variance structure. This diagnostic confirms that GARCH (1,1) is sufficient.

Figure 12: ACF of Squared Export Returns (Before vs After GARCH)

Figure 13 plots annual goods export goods log return alongside GARCH estimated conditional volatility. Returns surge dramatically in 2009(GFC) and 2015(commodity bust, early trade tensions). Critically, while returns swing negative during crises, volatility remain non negative measuring the magnitude of uncertainty not direction. The sustained elevation of the volatility confirms that the world has not returned to the low uncertainty regime of hyper globalization. Consequently, global trade is now characterized by structurally higher volatility, driven by geo political fragmentation, supply chain reconfiguration and financial instability.

Figure 13: Annual goods export goods log return vs. GARCH estimated conditional volatility

Returns computed as annual cross country mean of country pf goods export log returns conditional volatility derived from estimated parameters. Sample: N=7,455 country year observations.

Source: Author calculations using WDI data

In Summary, the univariate analysis confirms three critical facts: Volatility is time varying and persistent in trade and gdp flows especially in goods exports where shocks exhibit long memory; Trade has become structurally more volatile since the global financial crisis while GDP volatility has declined creating an asymmetry in risk exposure; The GARCH (1,1) model is well specified as validated by ACF diagnostics and provide reliable conditional volatility estimates for each series.

4.8: Time Varying Elasticities and Dynamic Shock Linkages.

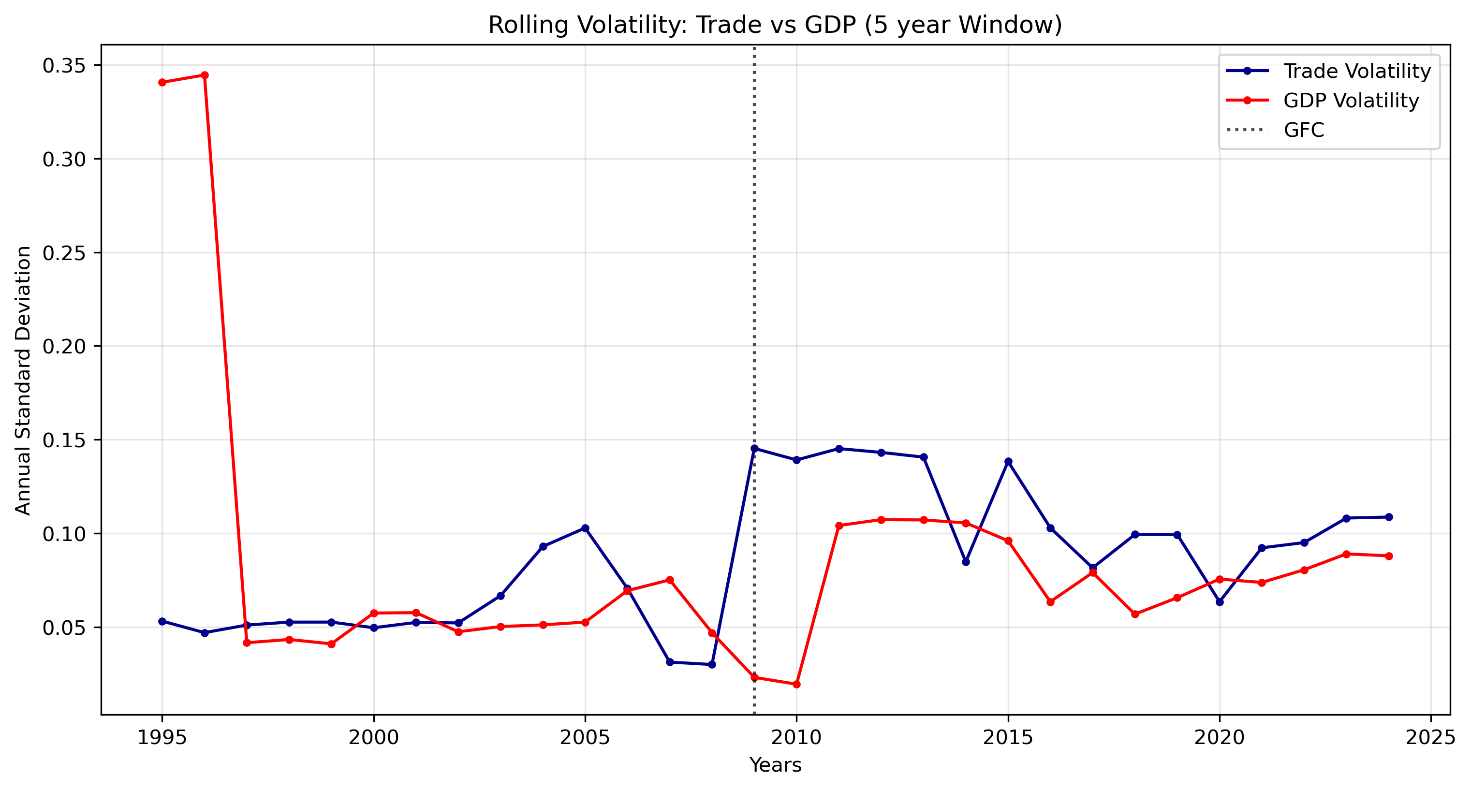

Having established that trade has become significantly more volatile than GDP since 2008 (Section 4.6), the next question is, how do shocks to trade and output co-evolve over time? To answer this, we move beyond static correlations and estimate time varying linkages using a transparent, non-parametric approach suited to annual macro data.

With fewer annual observations, parametric multivariate volatility models (like DCC-GARCH) are prone to overfitting and convergence issues. Instead, we follow the approach of Rancière et al. (2008) in macro finance. We estimate time-varying volatility as the 5-year rolling standard deviation of global average log returns, we further construct standardized shocks by dividing returns by their local volatility and compute a 5-year rolling correlation between these standardized series. This method isolates changes in co-movement strength from changes in individual volatility levels, revealing how the relationship itself evolves.

As confirmed by our Chow test (F = 15.4, p < 0.01), 2008 marks a decisive regime shift. In the post-crisis era (2009–2024), trade volatility surged by 87.4% from 0.060 to 0.112 while GDP volatility declined by 21.4%, from 0.098 to 0.077 (Table 15). This finding overturns the ‘Great Moderation’ narrative by Bernanke (2004). While domestic economies benefited from automatic stabilizers and service led growth, global trade absorbed systemic shocks aided by automatic stabilisers and supported by the growth of services. The result is a new macroeconomic reality where nations are internally stable but externally exposed.

Table 15: The Post-2008 Structural Break in Volatility

| Metric | Pre-2008 | Post-2008 | % Change | Economic Implication |

|---|---|---|---|---|

| Avg.Trade Growth Volatility | 0.06 | 0.112 | 87.4% | Trade became a macro source of global macroeconomic risk |

| Avg.GDP Growth Volatility | 0.098 | 0.077 | -21.4% | Domestic economies stabilized as external linkages became turbulent |

| Volatility Ratio (Trade/GDP) | 0.61 | 1.45 | +138% | Trade has become significantly more volatile than GDP |

Figure 14 reveal this stark regime shift. Before 2008, GDP growth was more volatile than trade, a reflection of domestic business cycle fluctuations. After 2008, this relationship flipped decisively, trade volatility surged by 87.4% (from 0.06 to 0.112), while GDP volatility declined by 21.4% from 0.098 to 0.077. the most volatile years for trade were 2009(0.150), 2011(0.150) and 2012(0.140) all crisis or post crisis periods.

This divergence reflects a fundamental shift, domestic economies have stabilized through automatic stabilizers, service led growth and monetary credibility, while global trade has become the primary carriers of systemic risk. The year-to-year autocorrelation of trade volatility (0.63) confirms structural uncertainty driven by on-going supply chain restructuring of supply chain restructuring and geopolitical fragmentation.

Figure 14: Rolling Volatility: Trade Vs GDP (5 Year Rolling Window)

Annual Std.dev of trade and gdp log returns computed using a 5 year rolling window. Volatility series derived from country level data aggregated to global annual means. Sample: N =7,455 country year observations:

Source: Author calculations using WDI data